For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on tri-monthly basis.

根据 Fortune Business Insights 的报告,2022 年价值 944 亿美元的全球棉纱市场预计将从 2023 年的 828.1 亿美元扩大到 2028 年的 1006.8 亿美元左右,预计 CAGR 为 4% % 在估计期间。 估值上涨的原因被认为是影响成品纺织品质量的纱线的独特特性。

在纱线类型中,估计普梳纱部分在此期间显示出相当大的扩张,这是由于该产品用于制造羊毛线的增加使用。在估计期内,服装部门也将实现合理增长,这可归因于电子商务渗透率的提高、可支配收入的增加等。

为国内纺织行业的利益而增加的政府举措被视为推动棉纱市场增长的关键因素。 这些举措侧重于纺织行业的技能发展、基础设施建设和部门发展。然而,由于与合成纱线价格较低相比的价格竞争,行业扩张可能会受到阻碍。

亚太地区的棉纱市场份额预计在预测期内将大幅增长,这可以归因于人口增长和消费者支出增加对产品的需求不断增加。然而,据估计,欧洲市场在预测期内将实现有利可图的增长速度。 这是由多年来不断增长的原材料需求和产业用纺织品的兴起所推动。

全球阻燃服装市场 2023-2027 预计在未来五年内将增长 100104 万美元,在预测期内以 4.9% 的复合年增长率加速增长。

阻燃 (FR) 服装是技术纺织品领域的一部分,该领域是全球的阳光产业。

市场研究解决方案 Reportlinker 的“2023-2027 年全球阻燃 tecApparel 市场”报告提供了全面分析、市场规模和预测、趋势、增长驱动因素和挑战,以及涵盖约 25 家供应商的分析。

本研究确定可穿戴技术是未来几年推动阻燃服装市场增长的主要原因之一。 此外,通过零售和在线渠道不断增长的分销以及新兴经济体不断增长的需求将导致市场需求巨大。

一些领先的阻燃服装公司是 3M Co.、Ansell Ltd.、Arco Ltd.、Carhartt Inc.、Carrington Textiles Ltd.、Cintas Corp.、DEVA FM。 sro、DuPont de Nemours Inc.、Frham Safety Products Inc.、Honeywell International Inc.、Hultafors Group AB、Hydrowear BV、Kimberly Clark Corp. 等。

根据 IMARC Group 的一份报告,2022 年印度的纺织品回收市场规模达到 3.087 亿美元,预计到 2028 年将达到 3.75 亿美元,2023-2023 年期间的增长率(CAGR)为 3.4% 2028.

纺织品回收是对旧衣服、纤维废料、边角料等进行再加工和再利用的方法。这些材料通常来自地毯、轮胎、家具、鞋类、废弃衣服、毛巾和床单。

纺织品回收有许多环境和经济效益,包括降低水和土地污染水平、限制化学染料的使用、优化能源消耗、最大限度地减少对原生纤维的依赖等等。

模拟印度纺织品回收市场的关键因素包括对生态完整性服装的需求不断增加、可持续时尚的新兴趋势以及消费者对生产新服装对环境的不利影响的认识不断提高。

由回收纺织品、塑料和有机原材料制成的生态服装越来越受欢迎,这进一步促进了这一增长,这有助于限制浪费并最大限度地减少垃圾填埋场空间。

政府政策和非政府组织计划以及纺织废料数量的增加和回收技术的改进也在推动回收市场,除了各种技术进步和回收过程中日益自动化以及领先制造商的广泛研发之外。

2021 年全球智能和互动纺织品市场估计为 21.476 亿美元,预计到 2030 年估值将达到约 164 亿美元,从 2022 年到 2030 年的复合年增长率为 25.6%。智能和交互式纺织品是与边缘计算、云数据、人工智能 (AI) 和蓝牙低功耗 (BLE) 等技术集成的织物,可以监控和交流穿戴者的数据。

根据 Global Market Insights Inc. 发布的报告,在研发方面的投资激增,以制造能够在战争情况下提供伪装效果、智能感知和响应能力的装备精良的士兵制服,再加上面料中的智能技术,以实现更轻的负载和更少的设备,促进了智能和交互式纺织品在军事和国防应用中的使用。

军事用途的智能纺织品能够监测穿戴者的表现,并配备 GPS 系统、传感器和活动跟踪器,提供多种属性,即绝缘性能、防弹保护和防水面料。在这些因素的加速下,预计从 2022 年到 2030 年,军事和国防应用领域将以超过 28.5% 的复合年增长率大幅增长。

在区域格局中,预计到 2030 年,欧洲的智能和互动市场将出现大规模扩张,占据约 28% 的行业份额。

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on tri-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

JELLYFISH SWIMWEAR(Code: MT0123-01)

30 PANMURE ST

ROUSE HILL

2155 NSW

AUSTRALIA

PRODUCT: BATIK APPAREL

EMPERIL-COMERCIO INTERNACIONAL S.A. (Code: MT0123-02)

RUA NOSSA SENHORA ASSUNCAO 1

ESPRELA – TROFA

4785-177

PORTUGAL

PRODUCT: POLYESTER FABRICS

MAXI IMPORT AS (Code: MT0123-03)

BJORNERUDVEIEN 15

1266 OSLO

NORWAY

PRODUCT: UNISEX APPAREL

本会不负任何交易后果。

欲索取联络 ,请联络本会办事处,并注明代号。

Fact.MR 发布的关于纺织染料市场的最新见解预测,到 2031 年,该市场的估值将超过 80 亿美元。快速发展的时尚趋势正在刺激对时尚服装的需求,促使制造商采用新的色彩组合和设计,推动销售,预计 到 2031 年以超过 6% 的复合年增长率推动市场扩张该市场在过去 5 年取得了令人瞩目的收益,到 2022 年底接近 60 亿美元。在此期间,年增长率约为 5%。 制造商预计将主要关注亚洲市场,印度和中国等主要国家将成为利润丰厚的增长中心。根据印度品牌资产基金会 (IBEF) 的数据,印度纺织业在 2018-19 财年占工业产值的 7%,预计到 2027 年估值将超过 230 亿美元。同样,根据纺织世界的数据,中国的化纤生产 超过 5000 万吨,占全球产量的 66% 以上。 这种趋势正在激励知名企业加大对这些市场的涉足力度。

市场研究的要点

• 对直接纺织染料的需求保持高位,到 2031 年将超过 20 亿美元

• 到 2031 年,活性纺织染料将以约 7% 的复合年增长率实现最快增长

• 预计粘胶纤维染料的复合年增长率约为 6%

• 涤纶纺织染料增长迅猛,复合年增长率约为 7%

• 美国纺织染料销售额可能会增加,2021 年达到近 7 亿美元

• 到 2031 年,印度、韩国和澳大利亚的总收入将略高于 6 亿美元

• 中国纺织染料领域的收入将超过 20 亿美元

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on tri-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on tri-monthly basis.

MAXI IMPORT AS (Code: MT0322-01)

BJORNERUDVEIEN 15

1266 OSLO

NORWAY

PRODUCT: UNISEX APPAREL

TARGET CONTRACT SRL (Code: MT0322-02)

VIA MONTE ROSA 27

LIMBIATE (MI)

20812

ITALY

PRODUCT: WOVEN FABRIC

SIAM BUSINESS & TRADING CO., LTD. (Code: MT0322-03)

1011-5 SONGWAT RD.KHWANG SAMPHANTHAWONG,

KHET SAMPHANTHAWONG, BANGKOK

10100 THAILAND

PRODUCT: LADIES APPARELS

CHEMISETTE (Code: MT0322-04)

16 DE SEPTIEMBRE NO.621

MONTERREY NUEVO LEON

MEXICO

PRODUCT: LADIES APPARELS, LADIES UNDERGARMENTS

根据 Future Market Insights 的最新研究,尽管 2020 年增长放缓,但在 2021-2031 年的预测期内,全球二手服装市场销售额预计将以 11.2% 的复合年增长率增长。

2021 年,衬衫和 T 恤占据了 29% 的市场份额,原因是随着职业女性劳动力不断扩大,消费者偏好产生了变化。

该报告进一步指出,由于存在大量较低的社会经济消费者基础,巴基斯坦占南亚二手服装销售额的 40% 以上,而危地马拉在拉丁美洲领先,在预产期内占据超过 30% 的价值份额。

这一增长归因于终端消费者生活方式的变化,加上工业化、城市化、经济发展和全球化,在过去十年加速了时装业的销售,特别是在发展中的国家和地区。电子商务也改变了购物体验,超过 60% 的人选择通过在线平台购买产品、服务和获取商品。该报告进一步提到,ThredUP 和 Poshmark 等公司的存在将在未来几年推动对廉价和生态替代新衣服的需求。 在线分销渠道的扩张也将是兆头。消费者对在线转售平台的认知度不断提高,快速增长的在线初创企业提供二手品牌、设计师商品和租赁民族服饰,这进一步推动了二手服装市场的发展。

中国产业用纺织品行业在两年内增长了 12%。根据国家统计局的数据,2021 年 1 月至 2021 年 9 月,非织造布和帘子布产量分别下降 1.01% 和上升 29%。过去两年,产业用纺织品行业的营业收入下降了 14.74%,相比之下,前两年的平均涨幅为 10.78%。在前两年平均增长 14.12% 之后,他们的整体收入同比下降了 63.78%。营业利润率为5.25%,比上年下降7.11个百分点。 31家上市企业第三季度营业收入下降1.15%,整体利润下降33.59%。例如,运输车辆用纺织品和过滤纺织品领域的上市企业增长强劲。

前三季度,非织造布、特种纱、麻绳(索)、丝带出口增长6.91%。非织造布出口下降了 4.52%。出口量增长8.06%。工业用纺织品出口额增长39.74%。化纤无纺布防护服(含医用防护服)出口下降79.81%。

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on tri-monthly basis.

PT.SHAILENDRA TSHAI INDONESIA (Code: MT0222-01)

UDANG 3 MULTI KAVLING A 03/03/KEL, KADU

KEC.CURUG, TANGERANG, BANTEN 15810

15810 TANGERANG INDONESIA

INDONESIA, REPUBLIC OF

PRODUCT: BABIES APPAREL

COMERCIAL COPELEC SA (Code: MT0222-02)

AV 18 DE SEPTIEMBRE 688

CHILLAN CHILLAN

CHILE

PRODUCT: LADIES APPARELS

LUCKY STAR WEAVING CO., LTD. (Code: MT0222-03)

33/8, 33/11 MU4, OMYAI, SAMPRAN, NAKORNPATHOM

73160 THAILAND

PRODUCT: YARNS

2020 年全球产业用纺织品市场规模为 1903.3 亿美元,预计到 2028 年将达到 2858.8 亿美元,从 2021 年到 2028 年的复合年增长率为 5.15%。

Verified Market Research 的一份报告称,由于全球人口以惊人的速度增长,预计纺织品的增长将在预测期内激增,从而导致采用现代技术来促进成果。

该报告按材料(天然纤维、合成聚合物、金属、矿物、再生纤维)、工艺(机织、针织、无纺布)、应用(运输纺织品、医疗和卫生纺织品、工业产品和组件)分析了产业用纺织品市场) 和地理。

由于跨境需求高,技术纺织品的出口活动增加,有利于市场增长。

然而,与传统的低成本替代品相比,该市场的增长主要是由于产品成本高而受到阻碍。这主要是由于用于制造这些技术纺织品或在制造过程中使用的原材料成本上涨。

在全球范围内,公司正在扩大产业用纺织品领域;例如,去年,土工建筑材料制造商NAUE推出了可生物降解的无纺土工布Secutex Green。

Freudenberg Performance Materials Apparel 推出了适用于 Freudenberg Active Range 中所有类型运动服的新型高弹性和透气衬垫和胶带。

同样,全球科技集团 Freudenberg 收购了总部位于英国的 Low & Bonar PLC,这是一家生产技术纺织品的公司,收购金额未披露。

印度政府也准备通过 PLI 计划吸引对这一产品类别的投资。

根据最新报告,到 2027 年底,全球自适应服装市场价值预计将达到 4087.6 亿,复合年增长率为 4.1%。

适应性服装是专门为有不同程度残疾的人设计的服装,包括后天残疾、先天缺陷、先天性发育障碍和其他身体残疾。专门为满足这些群体的需求而设计的服装可以为在英国生活的许多人提供一种赋权感并提高生活质量。不幸的是,对于有学习障碍的人来说,适应性服装通常是有这种类型障碍的人最不希望购买或穿着的。但是,有一些选项可以为这些人在款式、合身性和功能方面提供更多选择,使他们能够购买外观精美且功能良好的物品。紧身裤、紧身衣、袜子和裤子都是适应性服装,适合那些可能难以每天走路、说话或执行普通任务的人。紧身裤和紧身裤是最容易穿脱的可穿戴服装类型之一,这要归功于它们紧贴身体的方式,并且可以根据个人穿着者的体型和尺寸进行塑造。适应性服装(例如这些特殊类型的服装)采用高质量、耐用的材料制成,可抗撕裂、撕裂和褪色。

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

2. To attack these trade practices through WTO cases and US trade law. NCTO supports passage of legislation by the US Congress to address China’s ongoing currency manipulation including the imposition of tariff sanctions on China’s exports to the US and allowing US companies to attack Chinese subsidies at their source through the use of countervailing duty laws.

3. A permanent textile safeguard in the Doha Round of trade talks to address the unique problems posed by China and other non-market economies.

4. Not to allow China additional access to the US market through loopholes in future trade agreements. Future success on trade liberalisation in this sector hinges upon the prevention of such loopholes being included in future agreements.

5. Finally is that the US should resist any pressure to lower US textile tariffs during the Doha Round negotiations.

It is the result of the first online bidding for next year’s quotas set by the European Union.

Nationwide, there are 20,047 companies eligible for joining the bidding, and 6,935 of them have received bidding permission numbers. Of the total of 5,284 companies that bid, 3,385 won contracts.

The bidding move was made upon the request of many textile manufacturers in China for a more transparent and fairer process. It will also help better manage exporters’ performance.

Another 12% of the total quotas will go through the bidding process next time. A special committee under the ministry has been set up to take charge of bid invitations. The majority of the export quotas, 70%, are allocated based on textile dealers’ shipments from the previous year.

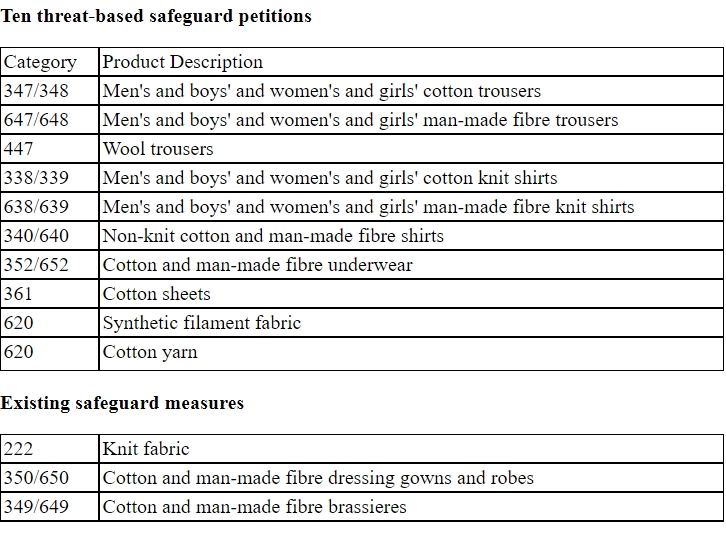

The government filed an appeal with the U.S. Court of Appeals for the Federal Circuit, asking it to overturn a decision by the U.S. Court for International Trade banning threat-based petitions.

Last year, textile industry groups filed a number of requests with the federal government to impose safeguard quotas on some types of Chinese textile imports. The safeguard quotas are designed to prevent Chinese textiles from overrunning the U.S. textile market and driving U.S. producers out of business.

Another group of U.S. companies, principally retailers and apparel makers, had filed suit asking the court to ban the government from considering those quotas purely on the basis of a potential threat rather than proven harm to the industry. Those companies are in favor of an open trade regime because it allows them to make clothing cheaper abroad and hence sell it for less in the United States.

The Court of International Trade’s decision came out of that lawsuit, which the federal government is now challenging.

In January, the United States imported more than $1.2 billion in textiles and apparel from China, up from about $701 million a year ago. Imports of major apparel products from China jumped 546%. Last January, for example, China shipped 941,000 cotton knit shirts, which were limited by quotas; this January, it shipped 18.2 million, a 1,836% increase. Imports of cotton knit trousers were up 1,332% from a year ago.

The 25 countries that are part of the European Union also registered big increases, importing about $1.4 billion worth of textile and apparel goods from China, up from about $975 million a year ago, a jump of 46% with Germany rising sharply by 46.39% in January. Germany was China’s fourth largest market in January.

The United States overtook Hong Kong and Japan to become the biggest buyer of Chinese textiles and apparels in January. Besides the United States, other countries that saw major increases in Chinese textile and apparel included EU countries, Turkey and Canada .Exports to Turkey increased 78.9%; those to Japan increased 11.9%; and products to Hong Kong increased 18.26%.

The top 10 markets for such Chinese exports in January include the United States, Japan, Hong Kong, Germany, South Korea, Russia, Italy, Australia, Britain and the United Arab Emirates. These countries comprised 65% of China’s total exports in textiles and apparels in January.

According to the latest consumer price index report from the US Department of Labour, clothing prices slipped 1% in July following a 0.9% slide in June and a 0.6% fall in May.

Those slides combined with earlier falls means clothing prices have fallen 3.2% from the year-ago period as firms who have switched their operations to countries with cheap labour pass on the savings of lower production costs.

Industry observers and economists say that move combined with greater competition at retail level has kept prices down with many shoppers tending to buy apparel from discount stores or shopping only during sale periods.

Commentators also point out that apparel prices could fall even further if trade chiefs were to increase textile quotas and reduce import duties as well as cut other strict trade regulations.

Organizer

Ministry of International Trade and Industry (MITI)

Eligibility

· Local companies with Malaysian equity of 51% and above

· Foreign companies incorporated in Malaysia (open category)

Judging Criteria

· Export Performance

· Market Penetration

· Product Development

· Market Operation

Benefits for Winners

· Exemption from the total participation fee of RM12,000 for 3 International trade fairs.

· Exemption from participation fee for exhibition space at the MEEC at Matrade headquarter and at Dubai for one exhibition session.

· Given space to advertise in Matrade’s export directory.

· Publicity of company profile of award winners on NPC, SIRIM, MITI and Matrade website.

Closing Date

31 July 2002 (Entry form and further details available at MKMA)

Anugerah Industri Selangor 2002

Anugerah Industri Selangor (AIS) is open to all companies operating in Selangor. The objective is to give recognition and also as a form of appreciation for outstanding achievements in Selangor.

1 Selangor Product Excellence Award

1 Selangor Quality Management Excellence Award

1 Selangor Export Excellence Award

There were six award categories. Award includes a trophy, certificate, eligible to use the award logo for 3 years and publish company particulars on SSIC website. Closing date for application is 31 July 2002. For further details please contact Ms. Zalina Mat Nasir (Tel : 03-5510 2005 / 5511 7988)

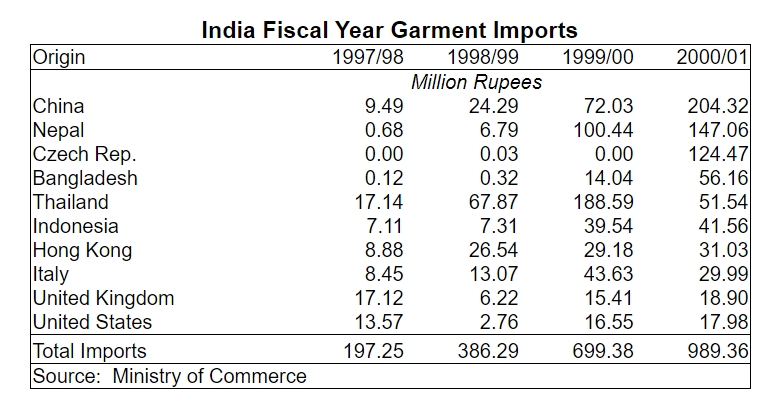

Making the condition worse for the domestic industry is the falling demand for Indian garments in the international market. According to the Apparel Export Promotion Council (AEPC), garments exports from India to quota countries during the month of November showed a decline of 9.19% in terms of quantity to 82 million pieces from 90.3 million for the same period last year. In value terms, however, the decline has been 15.71% to US$ 274.8 million from US$ 326 million last year. Garment exports in October had shown a slight recovery, registering an 11% increase in value terms to US$ 253.9 million as compared to US$ 228.8 million a year ago.

Exports during the April-November period of 2001 increased by a marginal 1.65% in terms of quantity to 635 million pieces. However, they posted a decline of 7.40% in terms of value to US$ 2314.7 million over the same period last year. When compared to November 2000, garment exports to the US increased by 10.86% in terms of quantity to

23 million pieces, but registered a decline of 15.50% in terms of value to US$ 116.6 million as against US$ 136 million in 2000.

Garment exports to the US during April-November amounted to 191.3 million pieces valued at US$ 1128.8 million, representing growth of 4.76% in terms of quantity but a decrease of 10.02 % in terms of value.

Exports to the EU during November showed a decrease of 15.50% in terms of quantity and 15.34% in terms of value, while exports to Canada decreased by 14.29% in quantity terms and 20.67% in terms of value. Readymade garment exports to the EU during April-November amounted to 400.5 million pieces valued at US$ 1048.3 million, representing an increase of 1.19% in terms of quantity but a decrease of 3.89% in terms of value.

From the beginning of the calendar year until November, overall readymade garment exports to the restricted countries registered a decline of 1.93% in terms of quantity to 954.2 million pieces compared to 8.80 % in terms of value to US$ 3477.5 million.

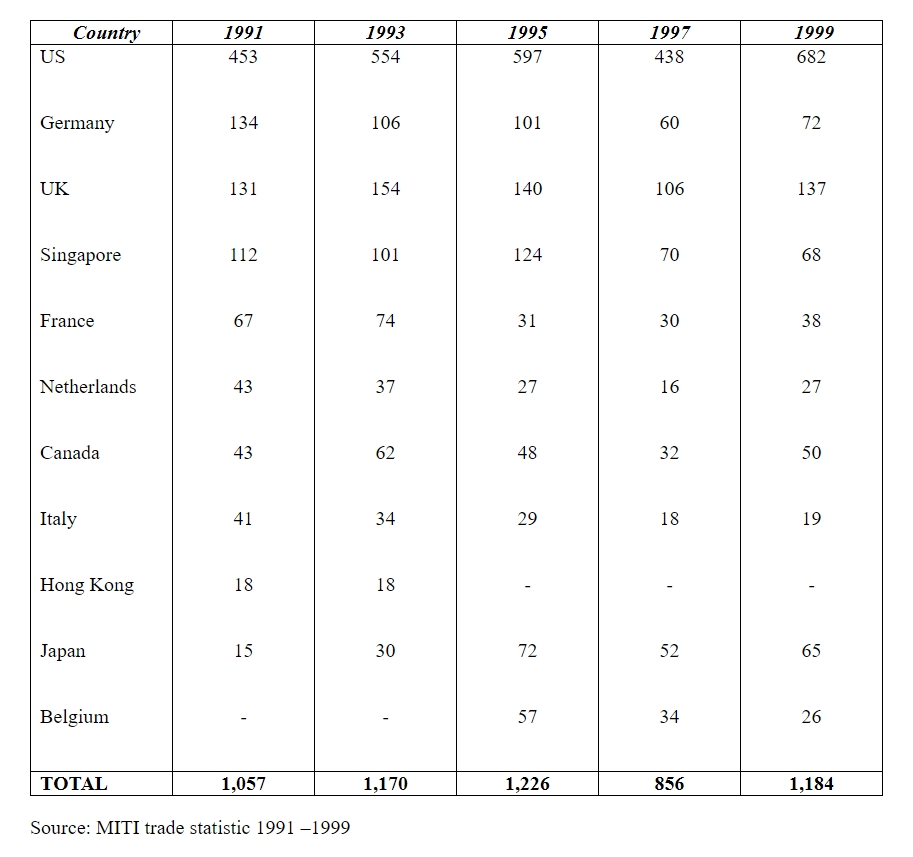

The above table shows that there has not been a significant change in the ten most important export-markers during the period 1991 – 1999. In other words, Malaysian apparel producing firms hardly diversified their most important export markets. Most exports of apparel go to the North American market, whereby Canada only plays a limited role. The share of exports to the US has been about three-quarter (SITC code 841 – 844), with the exemption of 1991, when exports to the United States accounted for half of the total exports. Exports to the EU have accounted about 40 percent of total exports during the period 1991 until 1997. In 1999 these exports, as a share of total apparel exports, dropped to about 28 percent.

The results of the key indicators merely give a rough picture of the respondents. This is due to a lack of accuracy and reliability of obtained information, which seems to reflect the sensitivity of certain subjects for apparel producers. Besides, data collection in the interviews regarding key indicators was based on 1997 with the aim to retain consistency in the ongoing research of Malaysian apparel producers. Many respondents pointed out that this turbulent year was not representative with the impact of the crisis. Moreover, some small firms with more than one establishment often did not break down the overall turnover into that of the different establishment.

Data regarding value added (value added is measured as the real value in RM a producer adds to a product: turnover ? input prices.) have also proved to be unreliable. It seems to be a measurement of little concern to most producers, because only 30 percent of the respondents had some kind of calculation for that and the figures vary from 14 to 75 percent of turnover. The aims of IMP2 regarding higher value added apparel might seem rather difficult to reach with such a low awareness of the principle. This lack of awareness could hinder measurement and evaluation of the degree of upgrading. Without past data it will be hard to determine if the industry is making any progress in this respect.

II. Employment

The average number of workers in the interviewed establishments is about 192. Survey shows that there is no tendency foreign companies setting up large-scale factories for assembly activities with many workers.

The number of workers was divided into a production and non-production segment, whereby the latter included personnel in management, administration, sales etc. The average share of non-production workers in total employment is rather high: 18 percent. In Penang it was below average: about 16 percent (43 non-production workers and 264 production workers). Firms in Selangor on the contrary, have a slightly higher share of non-production workers in total employment: nearly 19 percent (17 non-production workers and 91 production workers). This outcome is partly influenced by the fact that two of the respondents were a domestic headquarter in Selangor and had recently shifted to buying their items instead of producing them. This resulted in the absence of production workers.

III. Age

Regarding the age of the establishments, the average is 15 years in both Penang and Selangor. This implies that there is not such a high establishment/company turnover. However, according to most respondents and institutions, the recent crisis in 1997 has caused a shake out, in which many weaker producers had to end operations. In future, the trade liberalization in ASEAN is expected to have a similar impact. Unfortunately, in Malaysia there is no statistical data available on closed-down companies (or factories). Otherwise, there would have been more opportunity to bring some dynamics into these statistics.

IV. Ownership

About 76 percent of the establishments are domestically owned. The remainder consists of joint venture (13 percent) and foreign owned producers (11 percent). More than three-quarter of those establishments with foreign participation is exporting its total output and, according to expectations, 70 percent of them are located in Penang.

More than three-quarter of the foreign investments was already done in Malaysia before 1990. Since the Malaysian apparel industry is confronted with a changing competitive base, it seems that in the course of the 1990?s fewer companies still consider it as a good base for overseas apparel productions. The origin of joint venture capital is Europe in 50 percent of the cases and USA in only 17 percent. In the balance of 33 percent of cases capital is originated from the Newly Industrialized Countries (NICs). In establishments with full foreign ownership the NICs have a stronger foothold with 50 percent. Both Singapore and Hong Kong are represented in one establishment, while only two establishments have their HQ in Taiwan. Again the European countries take a strong position with 38 percent (UK, Sweden). The minor role of the USA in foreign establishments is striking. This may well mean that in general, US companies prefer to focus more on subcontracting and in later section regarding buyers, this will further be examined.

V. Products

Apparel producing establishments in Selangor are on average producing about four different items, whereas firm in Penang seem more specialized with an average of only two items in their production process. This pattern could be interpreted from both a positive and a negative side. First by specializing in certain product a producer can improved its competitive position by focusing on only one or a few products. The workers become very skilled in the production and assembly and a firm becomes a desirable supplier of its items through creation of knowledge and expertise, which enable improved product quality and quicker delivery time. On the other hand, more specialization could imply more vulnerability in a changing environment. If a producer decides to specialize in certain items, then at least it would be wise to keep some variety in the buyer base.

There is a clear regional specialization in certain items. First of all, Selangor has a strong focus on children?s wears as almost one-third of the establishments is producing this type of apparel. Then there is a broad second layer of knitted tops, (especially women’s) underwear, dresses and sportswear. Note however, that the lion share consists of knitted products with, on average, a moderate level of value added. The respondents in Penang seem to have other preferences as nearly half of the respondents produce outerwear, sportswear or both. Being more laborious in the production and using relatively better fabrics, outerwear is generally characterized by high value added. Therefore it is one of the items that make the producers eligible for the ?Pioneer Status incentive program’ of MIDA. Moreover, most of this outerwear will be exported, because in the tropical Asian countries the needs for outerwear (e.g. skiwear or winter wear) is much lower.

Compares to knitwear, woven items do not seem to be produced very much. It appeared that only three of the respondents are producing woven items. In other words, a remarkable share of 95 percent of the respondents was involved in the production of knitwear.

VI. Export

80 percent of all the respondents ? partly-exports its products. However, only 36 (20 producers) percent of all respondents is exporting its complete output, implying that the remainder of exporters (44 percent of all respondents) is only partly focused on foreign buyers or markets. In general, the average share of output that is exported is little more than two-third of total outputs. The two major export destinations for Penang apparel producers are the USA and the EU. This resembles national trade characteristics. Both markets are heavily restricted by quota. The peculiarity is that 32 respondents (71 percent of the exporting establishments) were producing quota items, but 36 respondents viewed quota as a problem in the last ten years. This would imply that four companies do not have a quota while they would like to have one. This does not automatically mean that they have applied for it. Many of the respondents said that it was not even worth a try to obtain ?more- quota. According to them the quotas were unequally divided, whereby the larger exporting companies with a long exporting history were always in favor to receive additional quota.

Producers in Selangor bring their products less far from the source and have countries like Indonesia, Philippines, Singapore and Japan as important regional consumer markets. Exporting apparel producers in Selangor have a high focus on certain markets: the average share of total exports going to Europe is 65 percent of total exports of the establishment. For Asia and America these figures are in both cases 67 percent.

VII. Buyers

As much as 93 percent of our respondents stated to have one or more buyers, accounting for an average of 90 percent of total output. Besides, a number of establishments produce for own brands as well. About 39 percent of the aggregate number of buyers has been further identified in terms of type, share of output, origin and whether or not they deal with an agent. When, for example, a producer said to have 15 buyers, he only identified five of them more thoroughly. Furthermore, some overlap occurs, as one buyer can obtain its items from more than one Malaysian producer. This has been the case with, for example, Adidas, Nike and Gap, which have spread their manufacturer base among many establishments. The more buyers a producer has, the less power each individual buyer can exert on a producer?s strategies. Naturally, this can only be the case if a producer has evenly spread its buyer base. The average number of buyers per producers is about 11.

This section will further be dominated by a categorization of buyers based on two different types of manufacturers. These two types are contract manufacturing and own brand manufacturing. The most common group of manufacturers is the contract manufacturers, whereas the group of own brand manufacturers has a much smaller share in Malaysian apparel production.

Contract Manufacturing

The buyers involved in Malaysian contract manufacturing can be divided into four major categories:

International Branded Companies

International branded companies have been categorized as follows: first there are the international sports and casual wear branded companies, such as Nike, GAP, Adidas, etc. Here, items vary from low to medium value items for the broad market (e.g. knitted shirts & tracksuits). The second group consists of companies like Nautica and Polo Ralph Lauren, for which higher value casual wear for more exclusive segments is produced. Thirdly, there are fashion houses carrying high value international designer brands such as Versace, Yves Saint-Laurent, Pierre Cardin and Boss. The last group includes the international jeanwear producers like Levi’s, Lee, Lois, Wrangler, etc. The first segment of buyers is the most common one, as half the total numbers of buyers identified belong to this segment.

Taking a closer look at the share in total output, the high-end casual wear companies have the largest share with nearly 30 percent on average. This could imply that this type of buyers prefers to have a limited number of core suppliers. In addition, with growth in demand they may be more willing to increase orders to existing suppliers instead of searching for new ones. By doing so, the buyer and manufacturer will better understand each other’s specifications and standards and build up a long-term relationship. In this sense it is kind of surprising that international designer brands have much less dedication in terms of share in total output. Although they tend to work with smaller batches, optimum quality standards and delivery times are crucial in this segment. Therefore, one should expect that this type of buyer prefers to have a frequent and dense relationship with the producer in order to guarantee its full attention to its orders. By having such a relatively small part (13 percent) in a firm?s output, they can exert less power to meet their high demands. On the other hand, generally producers seem to prefer spreading their risks by restricting the share to specific buyers in total output and not let it exceed a quarter of total.

Regarding the origin of international branded companies it will not be a surprise that the lion share (nearly two-thirds) is located in the US. Germany takes a second place and is responsible for 13 percent of total number of buyers. However, note that these shares are frequently dominated by just a small number of buyers. Main contributors in the US are Nike, FILA, GAP and Tommy Hilfiger, while in Germany Adidas has a central role in this respect.

Department stores

The department stores in the contract manufacturing are mostly the Japanese in Malaysia (Jaya Jusco, Isetan, SOGO) and to a lesser extent the local department stores (Metro Jaya and Parkson Grand). The latter generally focus on other market segments. Whereas the Japanese stores have more international quality brands, the Malaysian stores have a higher share of local and private brands.

Local branded companies

This is the third and last group of importance. It appears that they have a share of 8 percent in total number of buyers. Due to the limited size of the Malaysian market they lack the scale compares to many other buyers and often have a small share in manufacturers’ output.

Other buyers

The most prominent ones are the regional underwear brand companies, constituting 8 percent of the total number of buyers. Another group is that of Asian buyers (Giordano, U2, Urdan), which play a minor role compares to the former mentioned international buyers. They constitute only two percent of the number of buyers.

Own Brand Manufacturing

About 45 percent of the respondents are ?at least partially- own brand manufacturer. With OBM production, there is a different type of buyer in the scene. These companies have to deal with the final consumer and have to invest heavily in marketing, because the creation of brand loyalty takes at least a few years. This brand loyalty is especially needed to have guarantee and stable sales. Maintaining an own brand will also entail extensive market research to stay updated of the changing trends, whereas in the case of the contract manufacturers this is fully done by the buyers. More than one-third (35 percent) of the establishments with an own brand were operating its own shops or boutiques with the final customer as buyer. About 80 percent of these establishments still have some contract manufacturing besides their own brand with the main reason to spread risk and remain being updated on developments in the industry and markets. Having an own brand could vary from plain t-shirts with just an own label to whole product ranges with own brands. About 58 percent of total own brands’ output was sold at the domestic market in either department stores or own outlets or boutiques. Of those goods being exported, an important share is destined for Singapore and another part deals with intra-company transactions to other branches throughout Asia.

VIII. Suppliers

The number of suppliers used by our respondents was on average 18, divided into four main categories: fabric, threads, accessories and machinery. Regarding their relationship, 90 percent of the apparel manufacturers maintained mostly long-term connections with the suppliers. By far the most common reason for this was trust and a long-standing personal relationship. In general, it takes a few years to fully understand each other’s demands, capabilities and constraints. Particularly the last factor can be crucial when moving up to higher value added apparel. In case of increasing standard, the role and achievements of suppliers need to be reassessed and adjusted to a different level playing field. Whatever the value of the inputs, it is of pivotal importance that a supplier can meet the delivery times. Otherwise, the manufacturer would run the risk of serious disturbance of the production process due to lack of timely supply. The easiness of changing suppliers can also be linked to the quality of the product. Manufacturers of low value products tend to change the supplier base earlier in case of price differences, whereas high quality producer prefer to stick with their suppliers due to much more sophisticated requirements. In other words, the higher the quality, the more commitment there generally is between buyer and supplier. This is of course valid only for the high quality inputs that cannot easily be obtained elsewhere.

The large majority of the respondents stated they were fully dependent on foreign supply for their fabric and that either Malaysian suppliers could not provide them with a similar price/quality combination or the fabric are simply not available domestically. Nearly two-thirds of the respondents viewed rising input prices as a serious problem that has affected their business in the last ten year. According to some respondents it has proven to be very hard to maintain their quality-fabric suppliers. This has been especially apparent since the depreciation of the Malaysian Ringgit in 1997 to 3.8 RM/1 US$. Since then, some companies were forced to start searching for lower quality fabric for their apparel. Besides the depreciation of the Ringgit, there has also been a rather substantial increase in Taiwanese and Hong Kong output prices in the last few years.

IX. Organization of activities

Most of the respondents said to use subcontractors for at least one part of the production process. The share of companies using subcontractors is in Penang lower than in Selangor with 80 and 97 percent respectively. Out of the 50 respondents that were aware of their subcontracting network, only two (4 percent) stated to have subcontractors abroad and one of them did not indicate any local subcontractors. The remaining 49 producers have on average seven main local subcontractors, which are mostly located within proximity of the firm. By having the subcontractor in the area, the producer can better control the quality of the activities and delivery times are reduced.

Besides the larger number of main subcontractors, establishments in Selangor are also characterized by the contracting out of more activities (on average more than three activities), against two activities in Penang. Establishments in Selangor, more often contract out the production of entire garments to third parties. Especially the subcontracting including cutting is more frequently done by Selangor respondents than those in Penang. Seven of the respondents were actually third party CMT ? subcontractors for other local apparel manufacturers. Thereby, giving away practically every form of responsibility. In this case, the lion share of supplies will be delivered and the CMT producer only needs to cut and assembly the pieces of garment. It is not hard understand that this only gives marginal returns to the producer.

To initiate this focus program, US Customs sent letters to high volume importers and importers with a history of problems when importing ribbons and trimmings in mid-February. These letters set forth US Customs? concerns with improper classification upon entry into the US and with inadequate descriptions on the invoice. The letter states that on or about 17 June, US Customs will begin compliance review of ribbon and trimmings imports. This 120-day grace period is designed to allow importers, brokers and foreign manufacturers sufficient time to properly classify their goods and to modify invoice descriptions as necessary.

If problems are found during the reviews, the importers are likely to be referred to US Customs for further action. Such action could include increased entry reviews, cargo examinations, penalties or other remedial actions.

資料來源:馬來西亞工業發展局 (MIDA)

台灣在馬國紡織業最大的投資案是華隆公司,其他均以中小企業為主,經營規模都不大。由於勞工短缺,工資已沒有競爭力,早期到馬設廠生產成衣的台商多半已移到鄰近工資相對便宜的越南或柬埔寨,更多的廠商則移到大陸投資,在馬來西亞繼續經營成衣的幾乎沒有。至於投資其他紡織品的台商並不多,規模也不大,投資的地點也很分散,彼此間聯繫也很少。

由於台商在馬來西亞投資紡織業的廠商並不多,因此較難做深入的分析,目前先就華隆公司在馬來西亞的投資情況做介紹,以了解台商在馬來西亞紡織業經營的一些概況。馬來西亞的華隆公司成立於1989年,剛開始由布做起,慢慢向上整合到做人纖,目前有兩個廠運作,一在馬六甲,另一在森美蘭,一共雇用11,000人,資本額80多億台幣,但真正投入的資金有500億台幣左右。1998年營業額30億馬幣,最主要的產品是布,其他尚有聚酯粒、聚酯紗及短纖紗。華隆在馬的經營相當上軌道,營業額也年年成長,由1991年的1.2億馬幣成長到1998年的30億馬幣,8年間成長24倍,成績相當不錯。

華隆是屬於一垂直整合的紡織大廠,除了紡織最上游的人纖原料是向本地外商公司或向國外購買外,其他從人纖到成品布到個項紡織品華隆均在自己工廠生產。華隆採取一貫化生產的主要理由是可節省行政管理、運輸與包裝費,對競爭力的提升有幫助。華隆產品有95%外銷,內銷只占5%,雖然政府現在已放寬出口廠商的內銷限制,但華隆依舊以外銷為主。其外銷主要市場在大陸占30%,產品大多是聚酯紗;其他市場包括歐洲、中東、美洲、亞洲及台灣,比例都很平均。由於大陸市場所占的比重過高,亦受大陸內部政策及景氣好壞的影響,因此目前已著手進行市場分散策略,試圖將大陸出口比例降到20%左右。華隆產品有不少部份回銷台灣,均占出口值的10%左右,主要以布為主,因為馬國染整技術比不上台灣。華隆的台灣廠與馬來西亞廠雖然互相獨立,但彼此間仍會支援,包括產能上的互通、技術人員的派駐與受訓等。

華隆是馬來西亞最大的紡織廠,并沒有競爭對手,由於其產品大都出口,因此競爭對手仍以台商為主,這包括在台灣及在東南亞或大陸投資的台商。東南亞金融風暴對華隆公司的影響不小,雖然馬幣貶值有利出口,但相較之下,韓國、印尼及泰國貶值的幅度更大,因此造成華隆的競爭力下降。而馬國經濟衰退、銀行銀根緊縮,也造成華隆融資困難,新的貸款取得不易,影響工廠擴建與新投資計劃。華隆原先準備在1998年股票上市,但因受金融鋒暴影響,股價不振,因此延遲上市的時間,目前尚在等待時機。

台灣與馬來西亞紡織品的雙邊貿易,有些產品剛開始因為台商過去投資下游成衣業,帶動中、上游產品如纖維、紗及布的出口大增,但隨著馬來西亞勞工短缺及工資上漲等問題日益嚴重的影響,有些下游成衣業不是倒閉就是外移,或轉中、上游發展,使到台灣出口到馬來西亞的中、上游產品有逐漸減少的趨勢 (見圖二)。

圖二:台灣與馬來西亞雙邊紡織品貿易

Sri Lanka has agreed to tie all its tariffs for textiles and clothing in the World Trade Organisation (WTO) at rates of 0% for raw materials, 5% for fibres and yarns, 10% for fabrics and 17.5% for clothing products. Sri Lanka officials also decided to bring down a number of tariff peaks from the current level of 25 per cent down to just 10 per cent. In return the EU will suspend current quotas on imports of trousers, cotton blouses, cotton shirts and anoraks from Sri Lanka.

Certain products will be subjected to a double-checking system of import and export licensing in a bid to prevent third parties taking advantage of the agreement. EU officials also revealed that they had put in place a checking system for goods under current quota import restrictions with Bosnia and Herzegovina, in addition to the initial agreement out in place in November.

The agreement will also provide significant benefits to the European textiles and clothing industry. Under its terms, Bosnia and Herzegovina will not increase customs duties currently applied to textiles and clothing imports from the EU. Bosnia and Herzegovina will harmonise technical regulations and standards with those of the EU, in particular with regard to certification and labeling requirements. Both parties have committed themselves not to introduce or maintain non-tariff barriers on textile and clothing imports.

To prevent circumvention of textiles trade and to guarantee the origin of products from Bosnia and Herzegovina, the 11 most sensitive textile products for the EU (cotton yarn, woven cotton and synthetic fabric, pullovers, blouses, shirts, trousers, terry toweling, woven overcoats, suits) will be submitted to a double-checking systems (licensing).

An agglomeration of inter-linked or related activities comprising industries, suppliers, critical supporting business services, requisite infrastructure and institutions.

The industrial masterplan was again very theoretical, and we became very keen on finding out about cluster-based theory in the real world. Our interest became unraveling a cluster. We choose the textile and apparel industry because the University of Utrecht was already involved in a research project in this industry in Malaysia. Besides this, we were interested in this sector because it will always be there some way or another for the simple reason that ‘Everybody needs clothes’.

Questions we wanted to be answered through this research were for instance: What kind of actors (companies, institutions) operate in such a cluster? Do these actors co-operate with each other? And if they do, how was this relationship established and what does this relationship mean for the operations of a company? To answers these questions we formulated a questionnaire and came to Batu Pahat to uncover the depth and extent of this cluster and the linkages that are part of it.

All we knew about Batu Pahat when we came to Malaysia was that it is widely known as the textile town of Malaysia. Some people call it a ‘cowboy town’, some refer to it as the ‘Best Place’ in the world, but the truth lies in the fact that it is home to almost half of the textile factories in the country. The large amount of textile industries makes Batu Pahat the perfect area to conduct this research.

Firstly, the MKMA gave us an insight into how Batu Pahat turned itself into a textile town. We learned that the textile industry in Batu Pahat has a long history. In the 1950s a spinning mill was situated here. This mill was the start of a concentration of textile companies in this region. A lot of new textile companies were established by former workers of this mill. Nowadays especially the knitting segment is very strong represented in this area. Besides many small and medium sized enterprises, there are also a couple of very large players situated in Batu Pahat, e.g. Ramatex and the PCCS group. These companies are mainly export oriented and have also branches overseas, but are also seen as the frontrunners in the region for other companies. The opening of the southern branch of the MKMA was another boost for the textile industry in Batu Pahat. MKMA opened up a branch here because it felt that it could cater more for the welfare of the knitting related industries such as spinning, printing, and sewing. All these activities are well represented in Batu Pahat and the MKMA felt that a geographical closeness to the companies could help these companies in their representation to the government. In other words, being near the companies was a way to decrease the psychological distance to the government in Kuala Lumpur.

Batu Pahat can be seen as a special place for the textile industry in Malaysia. From one simple spinning mill the town has grown to an area with the largest concentration of companies in Malaysia that represent textile industry. In Batu Pahat almost all the activities in the textile commodity chain are carried out. Batu Pahat is a special place because the textile industry here is very linked with each other. The informal linkages are very tight in Batu Pahat. Most of the companies exchange information with each other and say that they help each other whenever they can.

These informal linkages were very striking to us. Textile manufacturers in Batu Pahat tend to “knit closely”. Instead of being organised in a formal matter through for instance an employers association, the contacts between the different companies occur mainly over dinner. Being invited to different of these lunches we could see with our own eyes how these contacts work. Events in the industry are discussed, day-to-day worries are shared, and new gossips cross the table. These informal contacts are in our opinion a good basis to share knowledge and information. We found out however that this does not occur on a large scale and could/should be improved. The owners of the different companies show reluctance when it comes to sharing knowledge. They always keep in mind that they are competitors. We think that when these entrepreneurs become less suspicious to one and another advantages can be gained for everyone. Two examples will make this clear.

Most of the companies we visited told us that they have a problem with finding skilled labour. A common reason for this is (according to them) the unattractive character of the industry. The general view of the industry is dirty, underpaid, long hours, and not glamorous at all (compared to electronics and automotives). Each of the companies tries on their own to get the right people, e.g. by importing foreign workers or shift operations to the kampong where there is still an unemployed workforce. Instead of solving the problem by them selves we think that when these companies join forces they should be able to overcome this lack of skilled labour. Training programmes could be initiated for instance on the workplace (financed by all companies), the general view of the industry could be improved by promoting it on universities and other training institutes. By solving the problem together time and money could be saved.

Another example is that companies complain about the locally produced fabrics. Local fabrics are often of a quality, which is not according the international standards. This causes problems for the garment companies as well for the fabric producers. The garment companies have to import their inputs and the local producers have to offer their products for a lower price. A solution could be a more intense co-operation between local suppliers and garment industries. With a more intense co-operation on product and process development quality could be improved and companies could get a better price for their products. The garment companies could get quality products in the vicinity instead of having to import it, which comes with uncertainties about delivery time and import regulations. In this way, local supply and local demand could become more linked in this way. Again, this would bring benefits for all participants.

Other problems the industry faces could also be solved more easily according to us when co-operation between the companies intensifies and trust increases. We see that the opportunity to co-operate is there (= informal contacts), but people do not make fully use of it. We even think that in order to survive the companies will have to co-operate more intensely in the future. Innovativeness is one of the keys to staying in business. Working together (as two people know more than one) on innovations is an opportunity to increase the competitiveness of the industry as well. Competition will increase and staying competitive will become harder and harder. Joining forces will become the way to survive!

At the moment we are working on our final report. Hopefully this will be finished at the end of July. This report will be send, of course, to the MKMA where everybody is free to take a look at it in the library.

Finally we would like to take the opportunity to thank all the companies who were willing to let us come to their factory and answer all of our questions. The interviews held have given us a lot of information about the industry to write our final report. We will remember Batu Pahat as the Best place!

(By Thomas Akveld & Pieter Liebregts, B.A. Candidates, University Utrecht, The Netherlands)

For more information, please log on to www.philau.edu/mba/tam.htm

or Email frumkins@philau.edu

Many of the products integrated in Stage Two were never under quota (and of course all of the products in the US Stage One integration were never covered by a quota). Despite the best effort to delay all important liberalization until the very end of the 10 year phase-out which is at midnight, December 31, 2004, there are some important consumer products that will be removed from quota protection in 2002 for WTO members countries creating new trade opportunities.

II. 2002 Quota Elimination Categories

Textile exporters are likely to be able to increase their exports to USA next year when quota affecting items are eliminated in line with WTO rules. Liberated items include gloves, gown, caps, suits, womenswear, neckties, fabrics and yarn.

The following categories will no longer be under quota in year 2002 :

331, 350, 359, 431, 459, 631, 649, 650, 659, 831, 833, 834, 835, 836, 838, 840, 842, 843, 844, 847, 850, 851, 858, 859, 222, 223, 621, 622, 810, 369, 464, 469, 666, 669, 670, 870, 870, 600, 606, 607, 800, 911.

III. Highlights for 3rd Phase Quota Removals

H Yarns – Several of the manmade fibre yarn categories – 600, 606, 607 will no longer

be under quota. This offers some opportunities.

H Fabrics – Category 222 which is cotton and/or MMF Knit Fabrics

Currently, major suppliers to USA are Canada (55%) Korea (7%), Taiwan (7%) and Hong Kong (6%)

In category 223 cotton and /or MMF non-woven fabrics. Major suppliers are Canada (22%) and Israel (19%)

H Apparel – Potential areas where US consumers are likely to increase their purchases

are Knit Shirts and Blouse (838) .

As a condition of doing business with Gap Inc., each and every factory must comply with this Code of Vendor Conduct. Gap Inc. will continue to develop monitoring systems to access and ensure compliance. If Gap Inc. determines that any factory has violated this Code, Gap Inc. may either terminate its business relationship or require the factory to implement a corrective action plan. If corrective action is advised but not taken, Gap Inc. will suspend placement of future orders and may terminate current production.

I. General Principle

The factory operates in full compliance with all applicable laws, rules and regulations of their respective counties.

The factory allows Gap Inc. and/or any of its representatives or agents unrestricted access to its facilities and to all relevant records at all times, whether or not notice is provided in advance.

II. Environment

Factories must comply with all applicable environmental laws and regulations. Where such requirements are less stringent than Gap Inc.’s own, factories are encourages to meet the standards outlined in Gap Inc.’s statement of environmental principles.

The factory has an environmental management system or plan.

The factory has procedures for notifying local community authorities in case of accidental discharge or release or any other environmental emergency.

III. Discrimination

The factory employs workers without regard to race, color, gender, nationality, religion, age, maternity or marital status.

The factory pays workers wages and provides benefit without regard to race, color, gender, nationality, religion, age, maternity or marital status.

IV. Forced Labor

The factory does not use involuntary labor of any kind, including prison labor, debt bondage or forced labor by governments.

If the factory recruits foreign contract workers, the factory pays agency recruitment commissions and does not require any worker to remain in employment for any period of time against his or her will.

V. Child Labor

Every worker employed by the factory is at least 14 years of age and meets the applicable minimum legal age requirement.

The factory complies with all applicable child labor laws, including those related to hiring, wages, hours worked, overtime and working conditions.

The factory encourages and allows eligible workers, especially younger workers, to attend night classes and participate in work-study programs and other government-sponsored educational programs.

The factory maintains official documentation for every worker that verifies the worker’s date of birth. In those countries where official documents are not available to confirm exact date of birth, the factory confirms age using an appropriate and reliable assessment method.

VI. Wages & Hours

Workers are paid at least the minimum legal wage or the local industry standard, whichever is greater.

The factory pays overtime and any incentive (or piece) rate that meet all legal requirements or the local industry standards, whichever is greater. Hourly wage rates for overtime must be higher than the rates for the regular work shift.

The factory does not require, on a regularly schedules basis, a work week in excess of 60 hours.

Workers may refuse overtime without any threat of penalty, punishment or dismissal.

Workers have at least one day off in seven.

The factory provides paid annual leave and holidays as required by law or which meet the local industry standard, whichever is greater.

For each pay period, the factory provides workers an understandable wage statement which includes days worked, wage or piece rate earned per day, hours of overtime at each specified rate, bonuses, allowances and legal or contractual deductions.

VII. Working Conditions

The factory does not engage in or permit physical acts to punish or coerce workers.

The factory does not engage in or permit psychological coercion or any other form of non-physical abuse, including threats of violence, sexual harassment, screaming or other verbal abuse.

The factory complies with all applicable laws regarding working conditions, including worker health and safety, sanitation, fire safety, risk protection, and electrical, mechanical and structural safety.

Work surface lighting in production areas – such as sewing, knitting, pressing and cutting – is sufficient for the safe performance of production activities.

The factory is well ventilated. There are windows, fans, air conditions or heaters in all work areas for adequate circulation, ventilation and temperature control.

There are sufficient, clearly marked exists allowing for the orderly evacuation of workers in case of fire or other emergencies. Emergency exit routes are posted and clearly marked in all sections of the factory.

Aisles, exits and stairwells are kept clear at all times of work in process, finished garments, bolts of fabric, boxes and all other objects that could obstruct the orderly evacuation of workers in case of fire or other emergencies. The factory indicates with a “yellow box” or other markings that the areas in front of exits, fire fighting equipment, control panel and potential fire sources are to be kept clear.

Doors and other exits are kept accessible and unlocked during all working hours for orderly evacuation in case of fire or other emergencies. All main exit doors open to the outside.

Fire extinguishers are appropriate to the types of possible fires in the various areas of the factory, are regularly maintained and charged, display the date of their last inspection, and are mounted on wall and columns throughout the factory so they are visible and assessable to workers in all areas.

Fire alarms are on each floor and emergency lights are places above exits and on stairwells.

Evacuation drills are conducted at least annually.

Machinery is equipped with operational safety devices and is inspected and serviced on a regular basis.

Appropriated personal protective equipment – such as masks, gloves, goggles, ear plug and rubber boots – is made available at no cost to all workers and instruction in its use is provided.

The factory provides potable water for all workers and allows reasonable access to it throughout the working day.

The factory places at least one well-stocked first aid kit on every factory floor and train specific staff in basic first aid. The factory has producers for dealing with serious injuries that require medical treatment outside the factory.

The factory maintains throughout working hours clean and sanitary toilet areas and places no unreasonable restrictions on their use.

The factory stores hazardous and combustible materials in secure and ventilated areas and disposes of them in a safe and legal manner.

Housing (if applicable)

Dormitory facilities meet all applicable laws and regulations related to health and safety, including fire safety, sanitation, risk protection, and electrical, mechanical and structural safety.

Sleeping quarters are segregated by sex.

The living space per worker in the sleeping quarters meets both the minimum legal requirement and the local industry standard.

Workers are provided their own individual mats or beds.

Dormitory facilities are well ventilated. There are windows to the outsides or fans and/or air conditioners and/or heaters in all sleeping areas for adequate circulation, ventilation and temperature control.

Workers are provided their own storage space for their clothes and personal possessions.

There are at least two clearly marked exits on each floor, and emergency lighting is Installed in halls, stairwells and above each exit.

Halls and exits are kept clear of obstructions for safe and rapid evacuation in case of fire or other emergencies.

Directions for evacuation in case of fire or accessible to all sleeping quarters.

Fire extinguishers are placed in or accessible to all sleeping quarter.

Hazardous and combustible materials used n the production process are not stored in the dormitory or in buildings connected to sleeping quarters.

Fire drills are conducted at least every six months.

Sleeping quarters have adequate lighting.

Sufficient toilets and showers or mandis are segregated by sex and provided in safe, sanitary, accessible and private areas.

Potable water or facilities to boil water are available to dormitory residents.

Dormitory residents are free to come and go during their off-hours under reasonable limitations imposed for their safety and comfort.

VIII. Free of Association

Workers are free to join associations of their own choosing. Factories must not interfere with workers who wish to lawfully and peacefully associate, organize or bargain collectively. The decision whether or not to do so should be made solely by the workers.

Workers are free to choose whether or not to lawfully organize and join associations.

The factory does not threaten, penalize, restrict or interfere with workers? Lawful efforts to join associations of their choosing.

Proposed Import Duty Deduction on Selected Textile Items

| HS Code | Description | Current Rate (%) | Proposed Rate (%) |

|

581100190 580121190 580122110 580124110 580125190 580131190 580135190 580190110 580190130 580190190 |

Quilted Textile Products Woven piled fabrics and chenille fabrics |

25 25 30 30 25 25 25 30 25 25 |

20 |

|

580211190 580211900 580219900 580220190 580220920 580220990 |

Terry toweling and similar woven terry fabrics |

25 30 30 25 30 25 |

20 |

|

580230130 580230300 580230900 580390100 |

Tufted textile fabrics |

25 30 25 30 |

20 |

|

580410110 58040190 580421110/30/90 580429110/30/90 |

Lace in the piece, in strips or in motifs |

30 25 30 30 |

20 |

|

630120100 630120900 630130100 630130900 |

Blankets and traveling rugs |

25 30 25 30 |

20

|

|

581010000 |

Embroidery without visible ground |

30 |

20 |

|

581091000 581092000 581099000 |

Cotton & other textile materials embroidery |

30 |

20 |

|

621210100 621210900 |

Cotton & other Brassieres |

30 |

20 |

|

621220000 |

Girdles and panty-girdles |

25 |

20 |

|

621230000 621290900 |

Corselettes |

25 |

20 |

|

621600100 621600300 621600900 |

Gloves, mittens and mitts |

25 |

20

|

|

630210000 630221000 630222000 630229000 930231000 630232000 630239000 630240000 |

Bed Linen |

25 30 30 30 30 30 30 30 |

20 |

|

630251000 630252000 630253000 630259000 |

Table Linen |

30

|

20 |

|

630260000 630291100 630291900 630292100 630292900 630293100 630293200 630293300 630293900 630299100 630299200 630299900 |

Toilet Linen and Kitchen Linen |

30 25 30 30 30 30 25 25 30 30 25 30 |

20 |

|

630311000/2000 630319000 630391000/2000 630399000 |

Curtain (including drapes) and interior blinds |

25 |

20 |

|

630411000 630419100/200 630419900 630491000 630492100/900 630493100/900 630499100/900 |

Furnishing Articles Bedspreads Mosquito Nets |

25 |

20 |

|

630510900 630520000 630532000/3000 630539000 630590000 |

Sacks and bags for packing of goods |

25 |

20 |

|

630511100 630611900 630612100 630612900 630619100 630619900 |

Tarpaulins, awnings, sunblind |

30 25 30 25 30 25 |

20 |

|

630631000 630639000 |

Sails |

25 |

20 |

|

63691000 630699000 |

Pneumatic Mattresses |

25 |

20 |

|

630790300 630790910 630790990 |

Canvas, webbing straps |

30 25 25 |

20 |

|

630800000 |

Woven Fabric and Yarn |

25 |

20 |

Lost stores and the health and whereabouts of employees have remained a primary focus for retailers with outlets in or near the World Trade Center. Fortunately, stores in the Centre itself were located at the base of the towers, making it easier for employees to escape. Gap Inc employees left safely, as did those of Marks & Spencer owned Brooks Brothers, which has a location across the street from the Center. Its site was later used as a rescue centre. However, Gap lost one Gap and one Banana Republic store housed in the World Trade Center. Boston-based TJX Cos has been hard hit ?the company lost seven female employees, who were on the American Airlines plane which crashed into the north tower.

Loss of Business

The economy of the US was already showing signs of distress in the months before the September 11 attacks. Sales figures on September 6 reported disappointing results. Federated reported a 2.6% decline, while Dillard posted a 2% drop. Saks Inc. posted 2% decline. Gap reported a 17% decline in spite of hard struggling. For most retailers, hopes of recovery collapsed after the attacks when consumer confidence plunged. Sara Lee Corp net income fell almost 5% in its fiscal first quarter as the company continues to face tough competition, higher raw material prices and a weakening economy.

With the consumer spending outlook becoming even gloomier, retailers are now requesting their suppliers to reduce or postpone their deliveries for the remainder of the year. Many Department Stores will also be canceling orders In New York, shopping plummeted.

Inevitably, clothing manufacturers in Asia, Mexico, the Caribbean and other countries, who mainly focus on the American market, will be hit by the fall in US consumption. Will European clothing imports compensate for this? Most probably not. European economy was slowing even before the terrorist assault on the US; now it could be heading into recession. Since the terrorist attacks, most economists have halved their forecast for euro-zone GDP growth in 2002, to just 1.1%.

Loss of Jobs

America’s fourth largest retailer, Sears, Roebuck and Co, announced to cut 4,900 salaried jobs in an effort to boost profitability at its 860 department stores. The job cuts represent 22 per cent of Sears’ salaried work. The reductions are about 2 per cent of the company’s total staff of 300,000 nationwide.

US based retail clothing Nordstrom Inc. has slashed its workforce by 3.6% due to sales slowdown. Following the September 11th attacks, Nordstrom which has 126 outlets in 25 states, has responded to declining sales by laying off 1,600 employees. In UK, unemployment rate currently stands at a 26-year low of 3.1 per cent, but job cuts are mounting.

Yarn manufacturer Parkdale America is to close two of its North Carolina plants because of high imports, an oversupply of yarn in the market and overall poor business conditions. Its decision will affect 84 workers at its plant at Belmont which produces cotton and polyester/cotton open-end yarns, and 34 workers at its plant at Kings Mountain which produces all cotton open-end yarns.

Loss of Confidence

US consumer confidence plummeted in October to its worst reading for more than seven years as widespread lay-offs made Americans increasingly gloomy. Last year, US retail sales of apparel and footwear totaled about $322 billion . However, many produces are now bracing themselves for a huge fall in sales as consumers’ confidence continues to wane.

UK consumer confidence, which has held up well for most of this year, slumped in October to its lowest level. The Consumer Confidence Barometer fell for a fourth consecutive month to -5 in October from -1 in September and a peak of +6 in June. Sharp drops in confidence after shocking events can be a poor leading indicator of future economic activity.

Change of Strategy

The terrorist attacks may also have some less expected longer-term effects. One of those could be the rise of protectionism, especially in the US. Harvard University researchers found that high levels of nationalism and patriotism are associated with support for protectionism. This finding suggests that sustained global conflict – which boosts nationalist fervour at home and abroad – could undermine support for free trade. Will the American textile and clothing industry accept without further campaigning the end of the ATC quota regime on January 1, 2005? Will they follow sensitive policies against China’s, the textile and clothing exporting giant, who in the next few months will be admitted to the World Trade Organization?

Change of Sourcing

Another longer-term effect of the September 11 attacks could be a change in the world map of clothing resourcing, and especially of Cutting, Making and Trimmin (CMT) activities.

This map has never been a pure reflection of wage and salary differences between countries, and not even of differences in total production costs. Otherwise, countries such as Egypt, Cambodia, Vietnam would be the leading clothing producers of the world while little if any clothing would be made in Italy, Hong Kong or Turkey. International clothing buyers and contractors, When looking for new sourcing locations, do not rush automatically to the cheapest possible labour countries. They also take into account the overall efficiency of a country, special import terms, lead times, the flexibility of factories, the availability of local fabric and accessories, the knowledge of foreign languages and the many parameters which define the “business climate” of a country.

Business climate factors which probably will be pushing companies to rethink their location strategy. Of course costs of clothing production will remain an important factor in deciding where to source. However more attention will probably be given to the general business climate in a country, including the security factor. Besides, American and European clothing groups will feel pushed to reconsider their choice whether to produce at home or overseas.

Change of Investment

Foreign investment invariably flows to countries where safe and high returns can be expected, that is preferably to North America, Western Europe and Eastern Asia. It generally shuns poor or dangerous countries. Another longer-term consequence of terrorism might be that domestic and foreign direct investment in the US itself and in some other countries will be deterred, leading to reduced output.

Worldwide Hit

Taiwan : US Apparel Exports Could Shrink By $100m

Exports are expected to shrink by 20 per cent or approximately US$100 million – although demand for army and medical textiles could increase. US is Taiwan’s largest outlet for textile and apparel products, accounting for 74 per cent of the island’s exports in the third quarter

In addition to subsiding market demand, higher rates for shipping services and war insurance costs on freight exports to the Middle East area are also hindering Taiwan’s textile and apparel exports. After the US, Saudi Arabia and United Arab Emirates are its largest customers.

On the positive side, US sourcing shifts away from Pakistan, Indonesia and other anti-US countries could benefit Taiwan.

Pakistan : Uneasy Position

Violent opposition from parts of its own population and revenge strikes from Afghan forces could be the price Pakistan has to pay for its co-operation in the international struggle against terrorism.

The ambitious Five Year Plan Textile Vision 2005 is aimed at reshaping the Pakistan textile and garment sector in a modern, dynamic industry. Government planners are dreaming of “a royal path” to modernization involving US$6b in investment over the period 2001-05. The chance that the sector can take this ‘royal path’ would considerably increase should the American-Pakistani cooperation against terrorism bring success (and a huge flow of American aid as ‘thanks’ ). It could however greatly diminish should internal political struggle – for and against the Taliban – result in chaos.

South Africa: US Clothing Sales Down

October is proving a quiet month for clothing exports from South Africa to the US following the September 11 attacks, with a number of orders.

Between March and September, clothing exports to the US from South Africa had increased by 45 % over the previous year. In March, South Africa qualified for preferential access to the US clothing market under the Africa Growth and Opportunities Act, which did away with import duties of between 15 per cent and 32 per cent for qualifying suppliers in nine sub-Saharan African countries. Following promulgation of the Act, South Africa is expected to improve on last year’s figure of $142 million dollars of exports to the United States.

Indonesia: Textile Exporters Face Huge Slump In Orders

Worries officials of the Indonesian Textile Association (API) say they expect the country’s 2001 textile export to decline 25% this year due to the economic slowdown in the main US market. Indonesia’s textile exports to the US topped $2.1 billion last year but that figure is expected to drop sharply in the next few months.

Several textile companies have already lost orders as a result of the US terrorist attacks, while others have been forced to slash their prices or risk losing the orders. About 26.3% of the country’s textile export goes to USA. Textile companies may decrease production first or reduce overtime work in order to survive the difficult time.

UK : Plain for Clothing Retailers

With the problems of M&S, the sale at a knock-down price of Bhs and the dramatic exit from the UK of C&A it is clear that the clothing sector has been among the hardest hit in Britain’s beleaguered retail industry. Nevertheless, even worse news is on the horizon. The latest five year forecast from retail consultancy Verdict says that life will get considerably tougher over the next few years.

For the last 2 months, we have honour to receive the Trade Commissioner of South Africa Embassy to present a talk on the African Growth and Opportunity Act (AGOA). Besides, 3 representatives from Jordanian Investment Board came all the way to reveal the mystery mask of Jordan. They were arranged to hold talks and meetings from Penang to Johor Bahru. Besides located in the Middle East, the conditions seems quite abundant supply of high quality manpower. Next, our Presidents were interviewed by journalist from Paris. They are from the London based Global Business Report to write a report on Malaysian Textile and Apparel Industry to be published on the winter issue of Fashion Business magazine.

Red Traffic Light

Further to the Budget 2002, we were informed by MIDA that they had consulted Custom not to lower the import duty of knitted products for the moment. However, related manufacturers needs to seek for new markets and adopt new measures before the red light turns green in the days ahead facing the unavoidable implementation of AFTA and WTO.

Red Hot Activities

Otemas, ITMA Asia, Factory Visits, Practical Trainings, Seminars, Meetings. We devote our best to members and we appreciate your full support to all activities.

Domestically, this will result in two irrevocable changes: first, the further opening up of the Mainland market and secondly, the progressive transformation of China into a transparent and rule-based market economy. Foreign companies may import most products into any part of China three years after accession.

The opening up of markets will speed up the institutional reform of the Mainland economy. The WTO system based on rules allows trade disputes among members to be solved fairly and objectively. Operating under this framework, China has to comprehensively improve its investment environment.

China is now the world’s fifth largest trading entity. According to a World Bank estimate, following its accession to the WTO, China’s share in world exports will almost double in five years: from 3.9% in 2000 to 6.3% by 2005. Economic reform and liberalisation will no doubt benefit the Mainland economy profoundly.

China : Cut Textile Tariffs

Upon becoming a member of WTO , China will cut import tariffs on industrial products to an average 12 % in 2002 from the current 15.3 % as it fulfils its World Trade Organisation commitments.

China would cut import tariffs on farm products to 16%, starting from January 1, 2002. Tariffs on textiles would fall to 18 %, on electronics to 11%, on machinery products to 10%, on cosmetics to 8 % and marine products to 14 %

Quotas on Chinese textile imports will formally end in 2005 as mandated under a WTO-wide accord, although a special import “safeguard” system will be in place until the end of 2008. China’s textile and apparel sector is one of the few that should see a clear benefit from WTO entry with the lifting of import quotas abroad. Chinese textile firms focused on exports will be best positioned to capitalise on the agreement.

China, now a member of the World Trade Organisation, also plans to become an ITA member, which means it would have to remove tariffs on all IT products by 2005. The average tariff on industrial products would be slashed to 9-10% by 2005.

US : Cutting off China Textile Quotas

According to a spokeswoman for the Ministry of Foreign Trade and Economic Cooperation (MOFTEC), the US government’s unilateral quota deduction on textile imports from China seriously violates the Sino-US bilateral textile agreement. She said that the US government, which recently decided to slash quotas on Chinese textile imports, had so far “provided no clear evidence” of the need to make the quota deduction which is estimated to be worth about $28 million.

She claimed the Chinese government has consistently implemented the Sino-US bilateral agreement, had developed bilateral trade relations on the basis of equality and mutual benefit and solved trade disputes with a practical and cooperative attitude. She added that MOFTEC was most unhappy with the situation and called on the US government to consider the overall Sino-US trade relations and correct its decision in order to ensure the smooth development of bilateral textile trade.

China vs India

China eyes 40% of world textile market by 2004 while India trying hard to manage its current 3% share.

If it is a race between the giants —India and China—for the global textiles market, the entry of China in the WTO will mean that India will have to think for a new strategy to compete or lose the race even before it has begun. Despite having similar resources and being clubbed in the same category for the race, one contender is capturing international market share while the other is losing ground.

With the growth of the world economy, it is expected that world textile trade would grow at 3-5 % every year. China which presently has a 19 % share in the world textile trade aims high and has set itself a target of achieving 40 % of global clothing market by the year 2004 dominating the scene completely. India on the other hand currently has 3 % share and nothing that it is doing can prevent the declining trends.

China – Advantage of Labour cost and Policy

According to Sudhanshu Bhushan, economist, Indian Cotton Mills Federation (ICMF): “the competitive advantage of Chinese textile industry arises from the low labour costs and economies of scale”.