For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on tri-monthly basis.

根据 Fortune Business Insights 的报告,2022 年价值 944 亿美元的全球棉纱市场预计将从 2023 年的 828.1 亿美元扩大到 2028 年的 1006.8 亿美元左右,预计 CAGR 为 4% % 在估计期间。 估值上涨的原因被认为是影响成品纺织品质量的纱线的独特特性。

在纱线类型中,估计普梳纱部分在此期间显示出相当大的扩张,这是由于该产品用于制造羊毛线的增加使用。在估计期内,服装部门也将实现合理增长,这可归因于电子商务渗透率的提高、可支配收入的增加等。

为国内纺织行业的利益而增加的政府举措被视为推动棉纱市场增长的关键因素。 这些举措侧重于纺织行业的技能发展、基础设施建设和部门发展。然而,由于与合成纱线价格较低相比的价格竞争,行业扩张可能会受到阻碍。

亚太地区的棉纱市场份额预计在预测期内将大幅增长,这可以归因于人口增长和消费者支出增加对产品的需求不断增加。然而,据估计,欧洲市场在预测期内将实现有利可图的增长速度。 这是由多年来不断增长的原材料需求和产业用纺织品的兴起所推动。

全球阻燃服装市场 2023-2027 预计在未来五年内将增长 100104 万美元,在预测期内以 4.9% 的复合年增长率加速增长。

阻燃 (FR) 服装是技术纺织品领域的一部分,该领域是全球的阳光产业。

市场研究解决方案 Reportlinker 的“2023-2027 年全球阻燃 tecApparel 市场”报告提供了全面分析、市场规模和预测、趋势、增长驱动因素和挑战,以及涵盖约 25 家供应商的分析。

本研究确定可穿戴技术是未来几年推动阻燃服装市场增长的主要原因之一。 此外,通过零售和在线渠道不断增长的分销以及新兴经济体不断增长的需求将导致市场需求巨大。

一些领先的阻燃服装公司是 3M Co.、Ansell Ltd.、Arco Ltd.、Carhartt Inc.、Carrington Textiles Ltd.、Cintas Corp.、DEVA FM。 sro、DuPont de Nemours Inc.、Frham Safety Products Inc.、Honeywell International Inc.、Hultafors Group AB、Hydrowear BV、Kimberly Clark Corp. 等。

根据 IMARC Group 的一份报告,2022 年印度的纺织品回收市场规模达到 3.087 亿美元,预计到 2028 年将达到 3.75 亿美元,2023-2023 年期间的增长率(CAGR)为 3.4% 2028.

纺织品回收是对旧衣服、纤维废料、边角料等进行再加工和再利用的方法。这些材料通常来自地毯、轮胎、家具、鞋类、废弃衣服、毛巾和床单。

纺织品回收有许多环境和经济效益,包括降低水和土地污染水平、限制化学染料的使用、优化能源消耗、最大限度地减少对原生纤维的依赖等等。

模拟印度纺织品回收市场的关键因素包括对生态完整性服装的需求不断增加、可持续时尚的新兴趋势以及消费者对生产新服装对环境的不利影响的认识不断提高。

由回收纺织品、塑料和有机原材料制成的生态服装越来越受欢迎,这进一步促进了这一增长,这有助于限制浪费并最大限度地减少垃圾填埋场空间。

政府政策和非政府组织计划以及纺织废料数量的增加和回收技术的改进也在推动回收市场,除了各种技术进步和回收过程中日益自动化以及领先制造商的广泛研发之外。

2021 年全球智能和互动纺织品市场估计为 21.476 亿美元,预计到 2030 年估值将达到约 164 亿美元,从 2022 年到 2030 年的复合年增长率为 25.6%。智能和交互式纺织品是与边缘计算、云数据、人工智能 (AI) 和蓝牙低功耗 (BLE) 等技术集成的织物,可以监控和交流穿戴者的数据。

根据 Global Market Insights Inc. 发布的报告,在研发方面的投资激增,以制造能够在战争情况下提供伪装效果、智能感知和响应能力的装备精良的士兵制服,再加上面料中的智能技术,以实现更轻的负载和更少的设备,促进了智能和交互式纺织品在军事和国防应用中的使用。

军事用途的智能纺织品能够监测穿戴者的表现,并配备 GPS 系统、传感器和活动跟踪器,提供多种属性,即绝缘性能、防弹保护和防水面料。在这些因素的加速下,预计从 2022 年到 2030 年,军事和国防应用领域将以超过 28.5% 的复合年增长率大幅增长。

在区域格局中,预计到 2030 年,欧洲的智能和互动市场将出现大规模扩张,占据约 28% 的行业份额。

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on tri-monthly basis.

JELLYFISH SWIMWEAR(Code: MT0123-01)

30 PANMURE ST

ROUSE HILL

2155 NSW

AUSTRALIA

PRODUCT: BATIK APPAREL

EMPERIL-COMERCIO INTERNACIONAL S.A. (Code: MT0123-02)

RUA NOSSA SENHORA ASSUNCAO 1

ESPRELA – TROFA

4785-177

PORTUGAL

PRODUCT: POLYESTER FABRICS

MAXI IMPORT AS (Code: MT0123-03)

BJORNERUDVEIEN 15

1266 OSLO

NORWAY

PRODUCT: UNISEX APPAREL

本会不负任何交易后果。

欲索取联络 ,请联络本会办事处,并注明代号。

Fact.MR 发布的关于纺织染料市场的最新见解预测,到 2031 年,该市场的估值将超过 80 亿美元。快速发展的时尚趋势正在刺激对时尚服装的需求,促使制造商采用新的色彩组合和设计,推动销售,预计 到 2031 年以超过 6% 的复合年增长率推动市场扩张该市场在过去 5 年取得了令人瞩目的收益,到 2022 年底接近 60 亿美元。在此期间,年增长率约为 5%。 制造商预计将主要关注亚洲市场,印度和中国等主要国家将成为利润丰厚的增长中心。根据印度品牌资产基金会 (IBEF) 的数据,印度纺织业在 2018-19 财年占工业产值的 7%,预计到 2027 年估值将超过 230 亿美元。同样,根据纺织世界的数据,中国的化纤生产 超过 5000 万吨,占全球产量的 66% 以上。 这种趋势正在激励知名企业加大对这些市场的涉足力度。

市场研究的要点

• 对直接纺织染料的需求保持高位,到 2031 年将超过 20 亿美元

• 到 2031 年,活性纺织染料将以约 7% 的复合年增长率实现最快增长

• 预计粘胶纤维染料的复合年增长率约为 6%

• 涤纶纺织染料增长迅猛,复合年增长率约为 7%

• 美国纺织染料销售额可能会增加,2021 年达到近 7 亿美元

• 到 2031 年,印度、韩国和澳大利亚的总收入将略高于 6 亿美元

• 中国纺织染料领域的收入将超过 20 亿美元

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on tri-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on tri-monthly basis.

MAXI IMPORT AS (Code: MT0322-01)

BJORNERUDVEIEN 15

1266 OSLO

NORWAY

PRODUCT: UNISEX APPAREL

TARGET CONTRACT SRL (Code: MT0322-02)

VIA MONTE ROSA 27

LIMBIATE (MI)

20812

ITALY

PRODUCT: WOVEN FABRIC

SIAM BUSINESS & TRADING CO., LTD. (Code: MT0322-03)

1011-5 SONGWAT RD.KHWANG SAMPHANTHAWONG,

KHET SAMPHANTHAWONG, BANGKOK

10100 THAILAND

PRODUCT: LADIES APPARELS

CHEMISETTE (Code: MT0322-04)

16 DE SEPTIEMBRE NO.621

MONTERREY NUEVO LEON

MEXICO

PRODUCT: LADIES APPARELS, LADIES UNDERGARMENTS

根据 Future Market Insights 的最新研究,尽管 2020 年增长放缓,但在 2021-2031 年的预测期内,全球二手服装市场销售额预计将以 11.2% 的复合年增长率增长。

2021 年,衬衫和 T 恤占据了 29% 的市场份额,原因是随着职业女性劳动力不断扩大,消费者偏好产生了变化。

该报告进一步指出,由于存在大量较低的社会经济消费者基础,巴基斯坦占南亚二手服装销售额的 40% 以上,而危地马拉在拉丁美洲领先,在预产期内占据超过 30% 的价值份额。

这一增长归因于终端消费者生活方式的变化,加上工业化、城市化、经济发展和全球化,在过去十年加速了时装业的销售,特别是在发展中的国家和地区。电子商务也改变了购物体验,超过 60% 的人选择通过在线平台购买产品、服务和获取商品。该报告进一步提到,ThredUP 和 Poshmark 等公司的存在将在未来几年推动对廉价和生态替代新衣服的需求。 在线分销渠道的扩张也将是兆头。消费者对在线转售平台的认知度不断提高,快速增长的在线初创企业提供二手品牌、设计师商品和租赁民族服饰,这进一步推动了二手服装市场的发展。

中国产业用纺织品行业在两年内增长了 12%。根据国家统计局的数据,2021 年 1 月至 2021 年 9 月,非织造布和帘子布产量分别下降 1.01% 和上升 29%。过去两年,产业用纺织品行业的营业收入下降了 14.74%,相比之下,前两年的平均涨幅为 10.78%。在前两年平均增长 14.12% 之后,他们的整体收入同比下降了 63.78%。营业利润率为5.25%,比上年下降7.11个百分点。 31家上市企业第三季度营业收入下降1.15%,整体利润下降33.59%。例如,运输车辆用纺织品和过滤纺织品领域的上市企业增长强劲。

前三季度,非织造布、特种纱、麻绳(索)、丝带出口增长6.91%。非织造布出口下降了 4.52%。出口量增长8.06%。工业用纺织品出口额增长39.74%。化纤无纺布防护服(含医用防护服)出口下降79.81%。

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on tri-monthly basis.

PT.SHAILENDRA TSHAI INDONESIA (Code: MT0222-01)

UDANG 3 MULTI KAVLING A 03/03/KEL, KADU

KEC.CURUG, TANGERANG, BANTEN 15810

15810 TANGERANG INDONESIA

INDONESIA, REPUBLIC OF

PRODUCT: BABIES APPAREL

COMERCIAL COPELEC SA (Code: MT0222-02)

AV 18 DE SEPTIEMBRE 688

CHILLAN CHILLAN

CHILE

PRODUCT: LADIES APPARELS

LUCKY STAR WEAVING CO., LTD. (Code: MT0222-03)

33/8, 33/11 MU4, OMYAI, SAMPRAN, NAKORNPATHOM

73160 THAILAND

PRODUCT: YARNS

2020 年全球产业用纺织品市场规模为 1903.3 亿美元,预计到 2028 年将达到 2858.8 亿美元,从 2021 年到 2028 年的复合年增长率为 5.15%。

Verified Market Research 的一份报告称,由于全球人口以惊人的速度增长,预计纺织品的增长将在预测期内激增,从而导致采用现代技术来促进成果。

该报告按材料(天然纤维、合成聚合物、金属、矿物、再生纤维)、工艺(机织、针织、无纺布)、应用(运输纺织品、医疗和卫生纺织品、工业产品和组件)分析了产业用纺织品市场) 和地理。

由于跨境需求高,技术纺织品的出口活动增加,有利于市场增长。

然而,与传统的低成本替代品相比,该市场的增长主要是由于产品成本高而受到阻碍。这主要是由于用于制造这些技术纺织品或在制造过程中使用的原材料成本上涨。

在全球范围内,公司正在扩大产业用纺织品领域;例如,去年,土工建筑材料制造商NAUE推出了可生物降解的无纺土工布Secutex Green。

Freudenberg Performance Materials Apparel 推出了适用于 Freudenberg Active Range 中所有类型运动服的新型高弹性和透气衬垫和胶带。

同样,全球科技集团 Freudenberg 收购了总部位于英国的 Low & Bonar PLC,这是一家生产技术纺织品的公司,收购金额未披露。

印度政府也准备通过 PLI 计划吸引对这一产品类别的投资。

根据最新报告,到 2027 年底,全球自适应服装市场价值预计将达到 4087.6 亿,复合年增长率为 4.1%。

适应性服装是专门为有不同程度残疾的人设计的服装,包括后天残疾、先天缺陷、先天性发育障碍和其他身体残疾。专门为满足这些群体的需求而设计的服装可以为在英国生活的许多人提供一种赋权感并提高生活质量。不幸的是,对于有学习障碍的人来说,适应性服装通常是有这种类型障碍的人最不希望购买或穿着的。但是,有一些选项可以为这些人在款式、合身性和功能方面提供更多选择,使他们能够购买外观精美且功能良好的物品。紧身裤、紧身衣、袜子和裤子都是适应性服装,适合那些可能难以每天走路、说话或执行普通任务的人。紧身裤和紧身裤是最容易穿脱的可穿戴服装类型之一,这要归功于它们紧贴身体的方式,并且可以根据个人穿着者的体型和尺寸进行塑造。适应性服装(例如这些特殊类型的服装)采用高质量、耐用的材料制成,可抗撕裂、撕裂和褪色。

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

For further information or news, please refer to MKMA Newsletters which are circulated to members only and published on bi-monthly basis.

• The per capita consumption of textiles for the year 2007 is 22.41 metres as against 21.49 metres in 2006 recording a growth of 4.28 %. On an average, a person purchased and used 0.92 metres more of textiles and clothing in the year 2007 than the previous year.

• On an average, an Indian spent Rs. 1488.39 on the purchase of textiles & clothing in the calendar year 2007, which is more by Rs. 97.30 over the previous year (a growth of 6.99 percent).

• The market size for textiles and clothing in India has stood at 25493 million metres in the year as compared to the previous year’s estimate of 24030 million metres (a growth of 6.09 percent).

• In value terms, the size of the Indian textile market was Rs. 1692952 million in 2007. The same for the year 2006 was Rs. 1555835 million, a growth of 8.81%).

• 3.22 percent of the Indian households have not purchased any textile items during this year while 14.64 percent of the households purchased textiles & clothing up to Rs. 1000.

• The highlights also include the gradual and most perceptible change in the fibre preference of the Indian consumers. Among all the fibre combinations, in 2007 too, the man-made and blended/mixed textiles taken together continue to grow, which has recorded a share of 60.08 percent in the total consumption in quantity. While Pure Cotton textiles & clothing has a share of 38.95 percent in the consumption, Pure Silk and Woollen products have a meager share of 0.62 percent and 0.35 percent respectively.

• Market for Shirt:

The total market size of readymade shirts has stood at 419 million pieces in 2007 as compared to 399 million pieces in 2006. The demand for shirt has thus gone up by 5.01 percent in 2007 over the demand in 2006.

The man-made and blended/mixed shirts are more popular with a demand share of 71.12 percent as against 28.88 percent of pure cotton shirts. The demand for cotton shirts during this period are estimated at 121 million pieces and man-made and blended/mixed shirts are estimated at 298 million pieces.

• Market for Trousers:

The total market size of readymade trousers is 314 million pieces in 2007 as compared to 292 million pieces in 2006. The demand for trousers has thus gone up by 7.53 percent. The trousers market shows a consistent and gradual increase in size.

The man-made and blended/mixed trousers more popular with a demand share of 73.25 percent of the market as against 26.75 percent of cotton trousers. The demand for cotton trousers during this period is estimated at 84 million pieces and for man-made and blended/mixed trousers it is estimated at 230 million pieces.

• Market for Jeans (Male):

The total market size of readymade Jeans (Male) has been estimated at 173 million pieces in 2007 as compared to 163 million pieces in 2006. Out of the above, the urban areas have a share of 43.35 percent and rural areas a share of 56.65 percent.

• Market for Jeans (Female):

The total market size of Jeans (F) has stood at 9 million pieces in 2007 as compared to 8 million pieces in 2006. The urban consumers mainly dominate in the usage pattern and this is close to 100 percent.

• Market for T-shirt (Male):

The total market size of readymade T-shirt (M) has stood at 179 million pieces in 2007 as compared to 165 million pieces in 2006 showing an increased demand for T-shirt (M) by 8.48 percent.

• Market for T-shirt (Female):

The total market size of readymade T-shirt (F) has stood at 13 million pieces in 2007 as compared to 11 million pieces in 2006 showing a growth of 18.18 percent.

• Market for Bedsheet:

The total market size of Bed Sheet has stood at 156 million pieces in 2007 as compared to 148 million pieces in 2006. The demand for Bed sheet has thus gone up by 5.41 percent in 2007 over the demand in 2006.

The cotton bedsheet is the popular with a demand share of 93.59 percent of the market as against 6.41 percent of man-made and blended/mixed bedsheet. The demand for cotton bedsheet during the period is estimated at 146 million pieces and for man-made and blended/mixed bedsheet it is estimated at 10 million pieces.

• Market for Towel/Terry Towel:

The market size of towel has stood at 400 million pieces in 2007 as compared to 387 million pieces in 2006. The demand for towel has thus gone up by 3.36 percent.

The total market size of terry towel has stood at 15 million pieces in 2007 as compared to 13 million pieces in 2006. The demand for terry towel has thus gone up by 15.38 percent.

Rules of Origin (ROO) are the criteria used to determine where a good has been made, for the purpose of ensuring that only the products of countries which are party to the FTA, enjoy tariff preferences (elimination/reduction of import duties).

Types of Rules of Origin (ROO)

Malaysia – Japan JMEPA

The Japan-Malaysia Economic Partnership Agreement (JMEPA) entered into force on 13 July 2006. For textile and apparel products, tariffs are eliminated with immediate effect.Rules of Origin for Textile and Apparel Products are as follows :

ASEAN-China FTA (ACFTA)

ASEAN-China FTA for Trade in Goods Agreement (TIG) was signed on 29th November 2004. Tariff on textiles and apparel will be fully eliminated by 1st January 2010 or 2012.

Product Special Rule (PSR) for textiles and textile products adopted from CEPT ROO. Exporters can choose the Alternative Rule of either

ASEAN-Korea FTA (AKFTA)

Negotiations for the AKFTA commenced in 2005. The Trade in Goods (TIG) chapter of the AKFTA entered into force on 1 June 2007, while negotiations for the Trade in Services chapter are still ongoing. Tariffs for most textile and apparel items are scheduled to be eliminated by 2009.

Product Special Rule (PSR) was adopted for textile products :

Malaysia – Pakistan FTA (MPFTA)

Malaysia – Pakistan Free Trade Agreement was launched on February 2005. Both countries signed an Agreement on Early Harvest Programme (EHP) on 1 October 2005 which came into force on 1 January 2006.

Tariffs on products identified for the EHP have been reduced to 0-5 per cent. Under the EHP, Malaysia offered a total 114 products covering yarn, clothing and textile products. Pakistan offered 125 products covering electrical appliances and machinery, plastics, chemicals, rubber and timber products.

Negotiations are on-going and expected to be completed by end-2007. One process Product Special Rule (PSR) applied to textiles and textile products. The process covers spinning, weaving, bleaching, dyeing, printing and finishing.

Below are the documents needed to enjoy preferential duty treatment under the abovementioned bilateral or multilateral agreements :

Malaysia and the US jointly announced the launch of negotiations for free trade agreement (FTA), on March 8 with formal negotiations on the FTA commencing in three months after the expiry of a 90-day consultation period with the US Congress and expected to be completed by early 2007.

US-Malaysia bilateral trade totaled US$44 billion (RM164 billion) in 2005 from which Malaysia had a trade surplus of US$34 billion (RM127 billion) and accounted for 16.8 percent of Malaysia’s global trade.

The US is Malaysia’s largest export destination, with total exports valued at RM105 billion (US$27.7 billion) or 19.7 percent of Malaysia’s global exports in 2005.

In terms of imports, the US is Malaysia’s second largest source of imports in 2005, with total imports valued at RM55.9 billion (US$14.8 billion).

As for investments, US remain an important source of foreign direct investment in the manufacturing sector in Malaysia. In 2005, the US was the largest source of foreign direct investments with total investments amounting to RM5.155 billion (US$1.4 billion), and representing 29 percent of total approved foreign direct investments in the manufacturing sector.

US-Asean Business Council Endorses US-Malaysia FTA Talks

Meanwhile the US-Asean Business Council also endorsed the FTA. The Council has been the leading private sector advocate behind the start of FTA talks with Malaysia. In December of last year, a Council delegation of 18 executives to Malaysia to encourage the start of FTA talks.

The US-Asean Business Council is the Secretariat of the US-Malaysia FTA Business Coalition.

The Coalition is co-chaired by representatives of several of the most recognised US brands, including American International Group, Cargill, Citigroup, Discovery Communications, Inc, Federal Express, General Electric Company, Intel Corporation and Oracle Corporation. Its Steering Committee is composed of the most influential American trade associations active in Washington.

With talks now announced, the full weight of this coalition will be brought to bear on achieving an agreement that can pass Congressional muster, and on building the necessary Congressional support.

Malaysia will join a list of 11 other countries with which Washington is currently negotiating free trade deals. FTAs already reached with Oman, Peru and Colombia is expected to receive Congressional consideration in the months ahead. Already under way are FTA negotiations with Panama, Ecuador, the United Arab Emirates, the five countries of the South African Customs Union, South Korea and Thailand.

Introduction

GST (goods & Service tax) is also known as Value Added Tax (VAT). The Malaysian government has decided to implement the GST in replacement of the current Sales & Service Tax system starting from 1st January 2007. However, many people still do not know what is GST. Some even never heard of the term GST.

MKMA has held 2 seminars in Batu Pahat and Kuala Lumpur respectively to educate our members and the public on the basic concept of GST with overwhelming response of 110 participants from 46 companies in total.

What is GST?

THE GST is a tax on domestic consumption. The tax is paid when money is spent on goods and services, including imports.

The GST charged to customers is called output tax and that paid on purchases by businesses is called input tax.

What happens to the current sales tax and service tax?

The current sales tax and service tax will be abolished by 2007. All persons who are at present licensed under the Sales Tax Act 1972 and Service Tax Act 1975 will need to register for the GST. The registration process is scheduled to start in July 2006.

How will it affect a supplier, manufacturer, wholesaler and retailer?

The supplier, manufacturer, wholesaler or retailer would have to pay for GST on his business purchases which are standard rated before selling his product. This means that he may have to carefully plan his cash flow and turn around time to cope with his business activity. Improper planning may lead to a huge cash flow deficit as it may take a few months before his product can be sold to the consumer.

GST is imposed on every stage of input, until the final goods is sold to the customer.

Registration for GST

Any person who is required to be registered needs to do so with the Royal Malaysian Customs Department. Registration can be done online or manually. A person who is not required to be registered can opt for voluntary registration and claim input tax credit on his purchases.

How is GST levied on imported goods and services?

For imported goods, GST will be levied together with the import duty and excise duty, if any, by declaring on the Import Declaration Form, and is payable at the time the goods are cleared from Customs control. The value of the imports should be in Ringgit.

In addition, a number of imported goods that are listed under the Import Relief Order are to be exempted from GST.

What about exported goods and services?

All goods exported out of Malaysia will be zero-rated. This means that the registered exporter does not collect GST on his exports but is able to claim credit for the GST that he has paid on his inputs. However, the exporter must retain supporting documents such as the Export Declaration Forms and copies of his invoices issued as evidence of export.

How to claim input tax credit?

The GST registered person, who is actually the supplier of goods or services, is eligible to claim input tax credits for any GST paid in the course of making the supply.

The net amount to be paid to the Customs is the difference between the input tax and the output tax. If the amount is positive, then that amount is payable to Customs. If it is negative, then a refund can be claimed. The reason for this is that GST, being a value added tax, is only payable on the portion of the value added to the goods or services.

How to prepare for GST?

Companies need to consider how to carry out the preparation for a smooth GST implementation and compliance. They may wish to seek professional assistance to review his current system to identify his business set–up and supply chain and to change or modify the system to be GST compliant by end 2006 without disruption to the day-to-day business activities.

The right accounting software package complete with GST capabilities is essential. It is important for the accounting software to be able to integrate all the relevant data from the modules of sales, procurement, inventory, receivables, payables and to generate accurate and complete reports and forms required by the Customs. Having an e-filing feature will be ideal.

To ensure efficient and effective implementation, a committee needs to be set up and headed by a senior person, ensuring all departments of the company understand what is required of them in order to comply with the GST.

Training is vital on the usage of the accounting software and GST implementations.

Conclusion

The GST legislation is expected to be passed sometime in March or April 2006. It is hoped that the Malaysian Government will start off with a low GST rate.

With a broader base for goods and services being subject to GST, the revenue for the Government is expected to be higher. The GST, being a consumption tax, is likely to have a temporary inflationary effect on taxpayers.

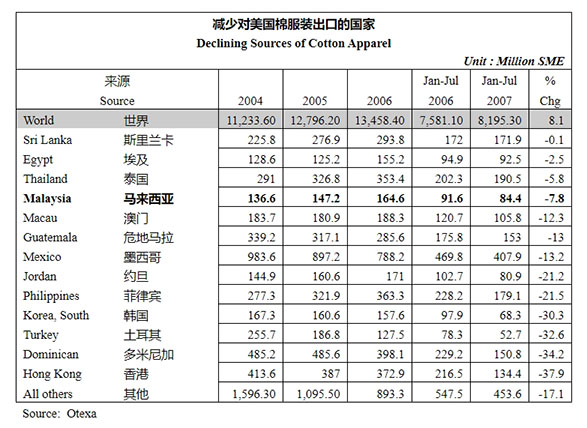

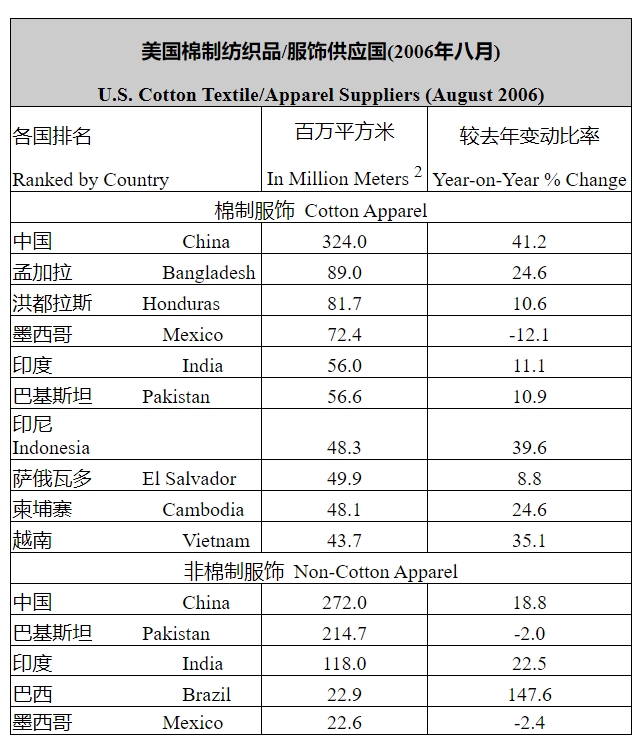

China’s role has definitely gained momentum, with imports surging 51.4 percent to 2.195 billion square meters. The second fastest-growing supplier is Vietnam increasing 31.4 percent to 393.9 millions square meters.

Within CAFTA, EL Salvador, Honduras and Nicaragua have emerged the winners as suppliers to the U.S. Indonesia, Bangladeshi and India are expanding their imports to the U.S., but Pakistan is losing market share. Imports from many of the traditional suppliers, such as Hong Kong, Turkey, South Korea, Malaysia, Philippines, Jordan and Mexico, have sharply declined.

China’s textile exports to most of these markets went up, with that to France and Spain jumping over 80% year on year.

From January to October, China’s provinces of Jiangsu, Zhejiang and Guangdong as well as Shanghai saw their textile exports exceed 10 billion US dollars.

The textile export volume of these four regions accounts for about 70% of China’s total textile exports.

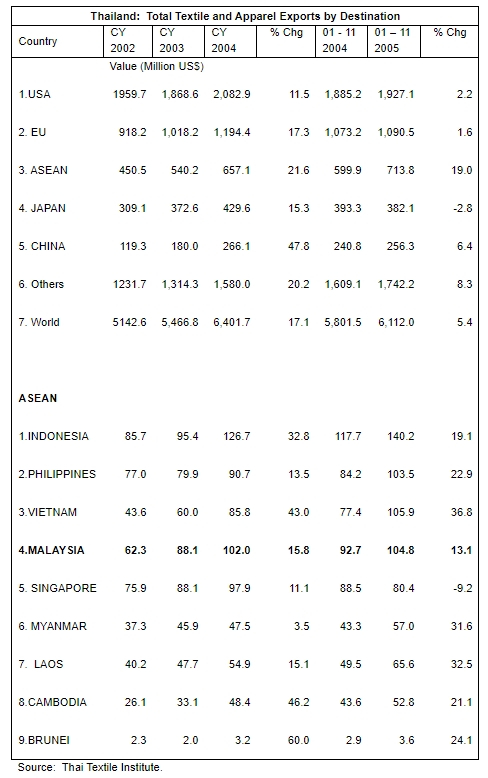

Much of the attention in the post 2005 quota period has been on the success of India, Pakistan and China in rapidly expanding exports of textiles and apparel. Without anywhere near the same attention, Thailand’s exporters have proved successful in expanding exports throughout 2005. The expansion has occurred despite little domestic production of cotton; nonetheless, cotton apparel exports have enjoyed the most rapid growth.

Thailand’s top export market is the United States; exporters have been successful in obtaining orders from all the major U.S. apparel brands. During the January through November time period, 31.5% of all exports have moved to the U.S., reaching 1.927 billion U.S. dollars and year-on-year growth of 2.2%. Despite this success, the Thai exporters and government are pushing hard for additional growth to the U.S. market. The Thai Garment Manufacturers Association and the Ministry of Commerce are jointly opening a U.S. office to promote one stop sourcing for U.S. apparel brands and retailing. The U.S. office will simplify orders, transportation, etc. Thailand’s exporters have also abandoned many of the cheaper, lower end products and moved into the high end products, which changes its competitors.

The European Union is Thailand’s second largest export destination. Export growth through November 2005 was limited to 1.6%, with shipments of 1,090 billion U.S. dollars. One reason for this is that EU import demand has been much weaker than in the United States.

One of the most important components to Thailand’s export expansion was the ability of exporters to benefit form the boom in domestic consumption of textiles and apparel through Asia itself. In 2005, the Asean trade block of nations was the third largest export market for Thailand’s textile and apparel. It also enjoyed the fastest growth. January through November exports to this trade block soared 19.0% to 713.8 million U.S. dollars and took 11.7% of all exports. Strong growth was enjoyed to most of the Asean trade block. The top markets were Indonesia, Philippines, Vietnam and Malaysia; double-digit export growth was noted to all four. Exports to Myanmar, Laos and Cambodia were smaller, but also enjoyed double-digit growth.

The Japanese market proved a disappointment in 2005. Despite Japan increasing the overall volume of textile and apparel imports, Thailand exports were unable to expand market share against China. January through November exports fell 2.8% to 382.1 million U.S. dollars. China emerged as a very important market itself. Through November 2005, China emerged as the fifth largest market, with exports expanding 6.4% to 256.3 million U.S. dollars.

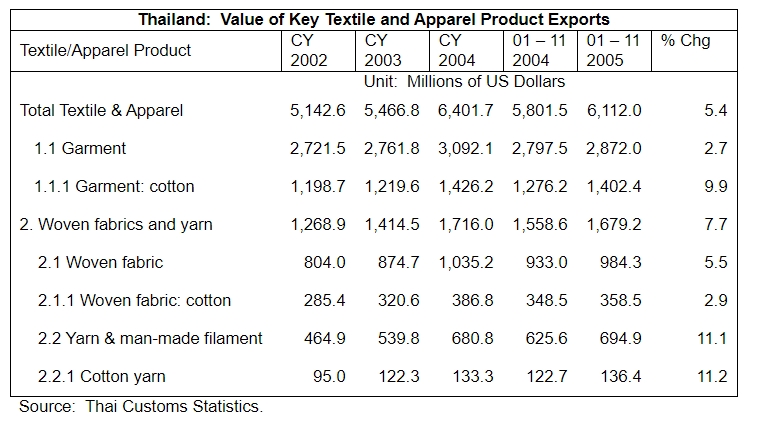

Cumulative January through November textile and apparel exports reached 6.112 billion U.S. dollars, reflecting year-on-year growth of 5.4%; apparel accounted for 3.163 billion of the total. Within the apparel sector, the strongest growth in exports came in co tton apparel. Cotton apparel exports expanded 9.9% from year-ago levels to 1.402 billion U.S. dollars, which compares to a 2.3% year-on-year decline in man-made fiber apparel exports to only 678.2 million U.S. dollars.

Strong growth has been noted in textile exports, woven fabric and yarn exports expanded 7.7% to 1.679 billion U.S. dollars. Woven fabric accounted for 984.3 million of that total, with cotton fabric exports totaling only 358.5 million U.S. dollars. Strong growth was noted in man-made fiber yarns, which expanded 11.1%. Household textile exports expanded to 219.2 million U.S. dollars.

US clothing demand grew vigorously in early 2005, helping to boost sales by major retailers such as Target and Wal-Mart. But the gains have gone mainly to foreign suppliers in Bangladesh, India and especially China.

In Latin America, Brazil exporters enjoyed growing demand in Argentina, China, Mexico, Paraguay, Uruguay and the Andean region. In Colombia clothing exports reached a record high while textile shipments soared. But Mexico faces tough competition in the US market from India, Bangladesh and other Asian suppliers.

EU15 output and orders fell in early 2005 as the stronger euro and quota elimination took their toll. The deficit rose for a fourth year as higher imports from Bangladesh, China and Pakistan offset modest export growth. But a new trade deal should stem the import surge from China. Meanwhile, firms are investing in China, India, Eastern Europe and North Africa. New EU states are investing in technical textiles.

In Japan, output continues to spiral downwards as foreign competition intensifies and firms invest in low cost facilities overseas. Exports from China, which supplies 80% of Japan’s clothing imports, soared by 21.1% in the first eight months of 2005. Yarn output rose by 23.8%, fabric by 16.7% and clothing by 19.4%. But success has led others to impose quotas on its exports.

Quotas have benefited Hong Kong as some operations have been moved back from China. But Hong Kong firms are investing in Cambodia, India, Indonesia and Jordan rather than China to avoid quotas.

In South Korea higher sales to China have only partly offset falling sales in the USA and many firms are turning to high-tech products. Firms in Taiwan have also suffered although some fibre makers are still investing. Indonesia has gained from quota elimination with exports up 32% in the first five months of 2005. But foreign direct investment has fallen.

Thailand and Malaysia have done better than expected with higher exports and output, despite relocation by some firms to Vietnam, Laos, Cambodia and Bangladesh. In Vietnam growth has been slowed by quotas on exports to the USA. Clothing exports from Bangladesh, helped by brisk sales in the USA, have done surprisingly well. But textile exports from India were sluggish, and much of the technology remains obsolete. Pakistan and Sri Lanka, by contrast, are enjoying brisk growth, despite Chinese competition.

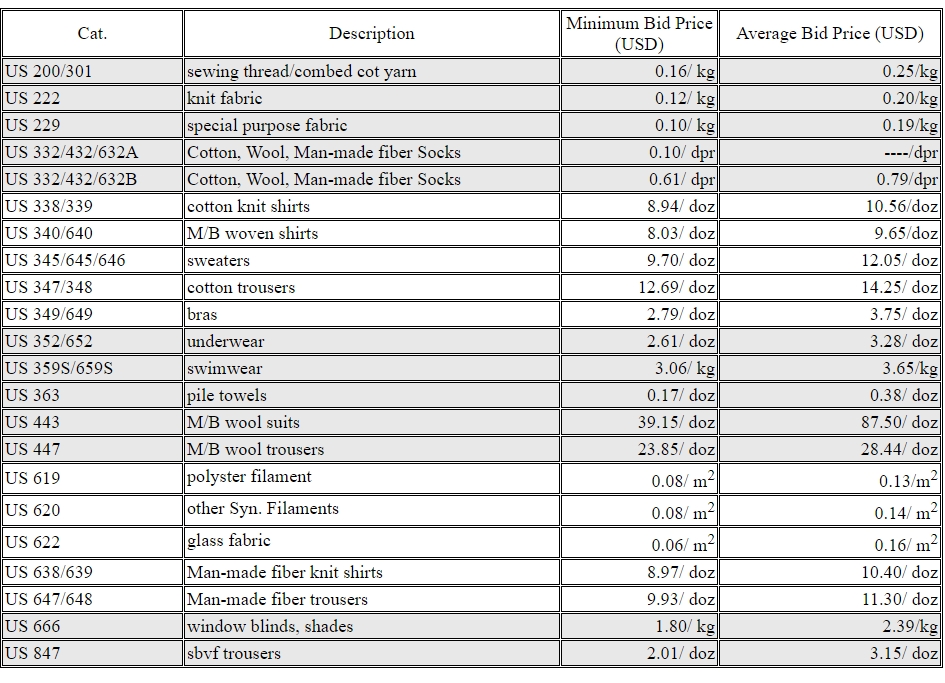

Qualified textile enterprises in China joined the bidding for export quotas on 21 categories of textiles to the United States for year 2006 on early December 2005. The competition was very heated. The bid result released on 10 December 2005 shown that quota was allocated to 3,734 textile enterpri ses. The final prices on most textile categories were much higher than the minimum bid prices. (To view full list of US quota bid result list, please browse MKMA homepage.)After seven rounds of talks, the United States and China in November signed a three-year agreement on textile trade, imposing quotas on Chinese textile products but clearing a major obstacle to bilateral trade.

A total of 21 types of clothing and textiles have been placed under the import restrictions. The agreement provides for a progressive increase in imports of major textiles and apparel products from China — by 10 to 15% in 2006, 12.5 to 16% in 2007, and 15 to 17% in 2008.

China has set aside 30% of US quotas for public bidding. The rest will be allocated to exporters based on their performance in the past year.

Yan Haiping, an export business manager, said the company believed bidding was important, although he knew US quotas would be mainly achieved from performance-based allocation.

Minimum bid levels range from 0.1 yuan (12 US cents) to 1 yuan per 1,000 kilograms and from 0.2 yuan per dozen to 12 yuan per dozen, depending on the product.

After companies get a quota, they can sign export contracts with importers in the United States.

Bid price to US Textile Quota Year 2006

As China reached agreements with both the European Union and the United States on quantitative limits on textile exports to the two markets, it would constitute double curbs on Chinese textile producers and exporters if the export tariffs were remained.

All export tariffs on textile products has been cancelled from Jan. 1, 2006.

China’s flexible tariff on cotton imports outside import quotas were created to maintain the stability of cotton prices in China, and the tariff rates would range from 5% to 40%.

The EU Generalized System of Preferences (GSP), implemented since 1971, grants unilateral tariff concessions to developing countries, that is, without any reciprocal concession from beneficiaries.

What does the new EU-GSP offer to Malaysia?

Ø consumer electronics (53.4% of total Malaysian exports to the EU in 2004),

Ø plastics and rubber (6.5%),

Ø wood (3.0%),

Ø clothing (1.8%)

Ø cereals and malt and starches (0.01%).

Accordingly, the share of Malaysia’s merchandise exports to the EU that is eligible for preferential tariff will rise from 16.2% in 2004 under the current EU-GSP to 80.9% under the new EU-GSP (assuming 2004 trade figures).

The two countries will lower their tariff upon Chinese textile goods to zero in 2010, and the Philippines will reduce its textile tariff in a similar way.

Indonesia, with its tariff rate against Chinese textile goods below 5%, will directly lower it to zero in 2009.

Vietnam’s previous textile tariff rate was as high as 36.6%, and it dropped to 31% after July 1, 2005, and will drop to 27.2% in 2006. It is expected to reach 26.6% in 2007, 22.8% in 2008, 19% in 2009, 12.6% in 2011, 5.8% in 2013 and zero in 2015.

Beginning from July 2005, China, Brunei, Malaysia, Indonesia, Myanmar, Singapore and Thailand gave tariff cuts to each other on 7,455 kinds of commodities. The practice was launched in compliance with the Trade in Goods Agreement of a Framework Agreement for Overall Economic Cooperation between China and the ASEAN countries.

By 2010, China and six old ASEAN member nations, including Brunei, Indonesia, Malaysia, the Philippines, Singapore and Thailand, will impose zero tariffs on most normal products, while China and the other four new ASEAN members of Cambodia, the Laos, Myanmar and Vietnam will do the same in 2015.

The China-ASEAN FTA has a population of 1.8 billion and two trillion U.S. dollars in gross domestic product (GDP). It will become the third largest global trading region after the European Union and the North American Free Trade Zone.

During the January-November period of 2005, China exported textile and apparel worth 5.08 billion U.S. dollars to the ASEAN, growing 22.4% year on year and accounting for 4.8% of China’s total textile export.

Meanwhile, China imported textile and apparel worth 620 million U.S. dollars from the ASEAN, growing 5.8% year on year and making up 4% of China’s total textile import.

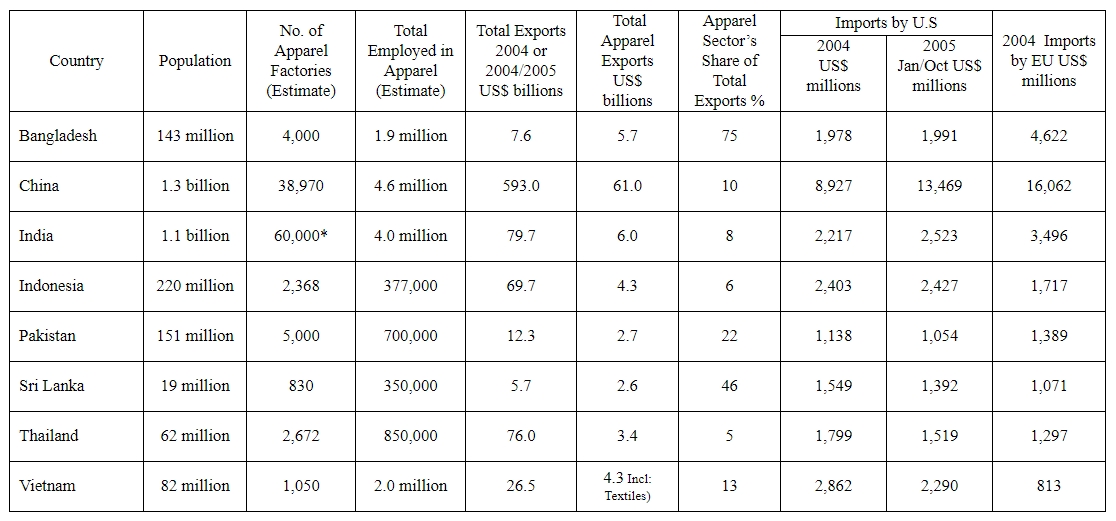

Eight major Asian textile and apparel players share many weaknesses creating hurdles to the growth of their share in the international markets.

These countries, covering nearly 50% of global exports of apparel and 80% of Asian apparel exports, have many common problems, including low- price image, environmental and social regulations, high electricity and fuel cost, dearth of trained manpower, infrastructure impediments and little exposure to high-tech machinery, said a study conducted by a Sri Lankan textiles and clothing sector writer, A H H Saheed, who is also a chartered marketer by profession. These countries are Pakistan, Bangladesh, China, India, Indonesia, Sri Lanka, Thailand and Vietnam.

The study, named Global Apparel Industry and Major Asian Suppliers, has discussed weaknesses of each of the Asian countries dealing in apparel industry separately.

Pakistan: Major weaknesses of Pakistan’s apparel industry include low-price image, reliability, marketing, environmental and social regulation and inadequate infrastructure, including power, water and the road network not able to provide foundation for a dynamic industrial sector.

Similarly, very expensive power, low grade technology leading to low productivity and poor quality, outdated machinery, lack of considerable upgradation of human resource skills and confusion in political, religious and social situation, including terrorism.

India: Again low price image is a major weakness like Pakistan and other Asian countries. Besides, buyer hardship and control, environmental and social regulations, narrow export base in garment as over 50% is confined to four products, relatively low technology, hardly available traditional tailoring background and automation in decentralized garment sector, inconsistent, low quality and productivity and a higher power cost in India’s power cost also hampering growth there.

As per ITMF – Study 2003, power cost in India is $ 0.08 per kw, higher comparing with other seven countries and China, Brazil, Korea, Turkey and the USA. Then India’s cotton yield is only 372kgs per hectare as compared with the world average 900-1000kgs per hectare. Low labour productivity, pro-employees labour laws resulting in unproductive employees union in India, which are mainly externally and politically motivated.

China: The quota restriction and safeguard measures from the US and the EU are described as major weaknesses of the apparel industry in China. Then wage rates in the apparel industry and other production costs, land prices, training, social fees and shipping costs are rising, Social responsibility/accountability and labour issues, low price image, buyer hardship, mass production/flexibility have been counted as some other major issues in China.

Bangladesh: Low-price image again emerges as a major weakness in Bangladesh. According to the writer, interest rate for long-term in Bangladesh is very hi gh, that is, 9-12%, as compared with 5-6% of competitors. Similarly, no fund for assistance to textile and apparel sector has been created and when it is coupled with the dearth of trained manpower of international standards and lower labour, the situation is translated into low productivity and inconsistency in quality. Then obsolete production technique, over-dependence on imports, especially woven fabrics, environment and social regulations are few other weak areas in Bangladesh. Particularly, reliability and lead-time in Bangladesh is high as 90-120 days and machinery is mostly outdated unable to keep pace with technological development. Finally, weak marketing and selling techniques had made impossible for any company to develop a brand or have any new market emerged.

Vietnam: In Vietnam product quality needs improvement, as technology and machines are 10-20 years old compared with regional countries, that has put the production costs very high something around 5-7% compared with competitors China, India, Bangladesh and Indonesia. The country imports fabric and accessories demand of the clothing industry and it lacks fashion design badly. High oil prices and being a non-member of the WTO is again a big challenge for its apparel sector.

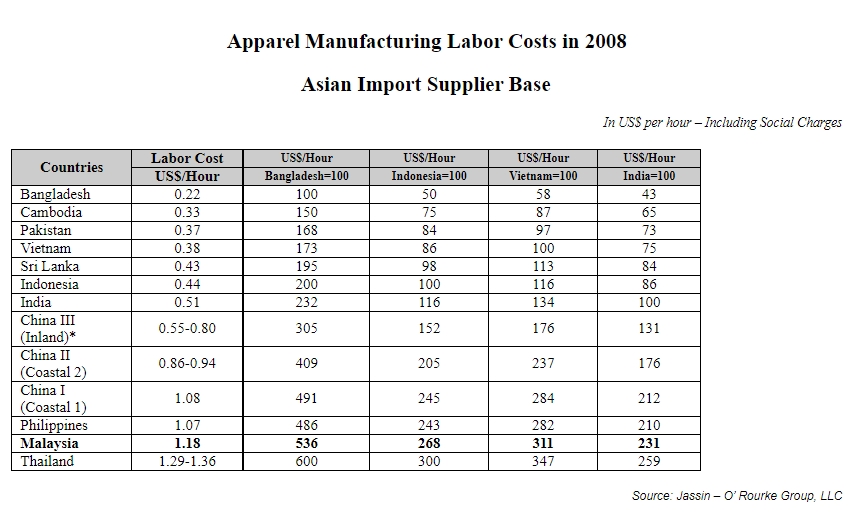

Thailand: According to the report, most export products of Thailand are commodity types, which are subject to fierce competition and have lower prices. Then the lack of variety and quality products due to shortage of technical manpower and modern technology is resulting in loss of competitive advantage compared with lower cost countries, especially in labour wage rate. The wage rate in Thailand is $1.24 per hour – higher than India, Indonesia, Sri Lanka, Vietnam, Bangladesh and Pakistan. Relying on imported raw materials, the domestic industry cannot supply material, especially quality and variety. High cost of production and difficult to get workers is another big issue there. There is a general lack of skilled people, particularly in the sewing industry, so productivity is not high and investments and industrial engineering are limited.

Sri Lanka: Continued civil war in the country significantly has suppressed the growth potential of the economy and adversely affected investor confidence. The apparel industry there heavily depends on imported raw materials, say 80%, ie, 150 million kgs of fabric are imported annually. The industry has not kept pace with the technological developments. The issue of longer leader times is also hampering growth there. The need to import fabrics results in longer lead times for the apparel industry. The average lead time – 8 weeks or more and lower labour productivity are big weak areas of the industry. The fall is attributed to lower capacity utilization, high labour turnover, absenteeism and under-trained employees and most factories lacks design and product development.

The domestic market there is relatively small with 19 million people and high electricity and fuel costs besides weak supply chain management are main stumbling block there.

Indonesia: In Indonesia, political instability and confusion in the political and social situation, including terrorism, are proving to be major hurdles facing the industry. The infrastructure needs improvement. The rising electricity and fuel costs, increasing trend of minimum wages coupled with low-tech textile and clothing industries is another weak area of the industry. Depreciation in rupiah has increased import costs and oil fuel prices. There is also an increase in the number of labour unions there.

The comparative data below shows some estimates of the size and scope of the apparel markets of eight of the major apparel-producing countries in Asia.

China, Bangladesh, India, Pakistan and Indonesia Takes the Lead

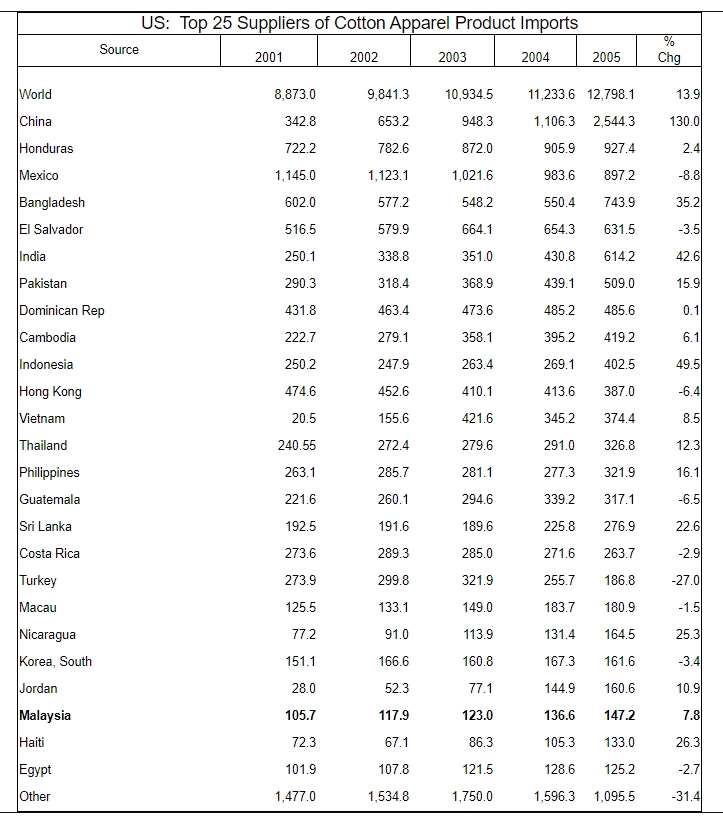

The U.S. imported 41.142 billion U.S. dollars worth of cotton apparel in 2005; this represented 10.01 percent growth in value terms. In quantity terms, the volume expanded 13.9 percent to 12.798 billion square meter equivalents. This was a record, and the import growth was up sharply from only 2.7 percent in 2004 and 13.9 percent in 2005. A clear pattern appears to have developed regarding retailers preference to source cotton apparel.

Despite the mid-year imposition of safeguard quotas on many key products, U.S. imports of cotton apparel from China expanded 130 percent to 2.544 billion square meter equivalents.

Despite duty-free access, the CAFTA/NAFTA region lost significant market share. In many cases, the wide array of obligations placed on these trade deals by the U.S. textile interests have significantly rendered them ineffective. Mexico actually fell to be the third largest supplier of cotton apparel for the first time and may soon fall behind Bangladesh.

U.S. retailers like Bangladesh for cotton apparel. With labor rates below China, its less-developed status and access to duty-free cotton, Bangladesh has carved out a significant market share. U.S. imports of cotton apparel from Bangladesh reached 1.684 billion U.S. dollars in 2005. Its products remain the cheaper, less valued items. In quantity terms, Bangladesh shipped 743.9 million square meter equivalents of cotton apparel to the U.S. This compared to Mexico’s 897.2 million square meter equivalents; however, in value terms, Mexico’s shipments were worth 3.987 billion U.S. dollars.

India exported 2.306 billion U.S. dollars of cotton apparel to the U.S. market, representing 43 percent year-on-year growth. In volume, exports reached 614.2 million square meter equivalents.

Pakistan was the seventh largest supplier to the U.S. in volume, with shipments of 509.0 million square meter equivalents; however, the value of these shipments were only 1.182 billion U.S. dollars, which reduced it to the twelfth largest supplier.

The big story of 2005 was the emergence of Indonesia as a top supplier of cotton apparel. In value terms, Indonesia was the seventh largest supplier, shipping 1.545 billion U.S. dollars worth of cotton apparel to the U.S. market, representing a 47 percent year-on-year increase. In quantity terms, Indonesia was the tenth largest supplier, with shipments increasing 49.5 percent to 402.5 square meter equivalents.

Another country that did not make the top suppliers in either quantity nor value measurements but gained significant momentum with retailers was the Philippines. Cotton apparel exports to the U.S. in 2005 reached 1.182 billion U.S. dollars, a gain of 15.56 percent, it was the fourteenth largest supplier, increasing shipments 16.1 percent to 321.9 million square meter equivalents.

Malaysia managed to maintain its share as the 23rd supplier and with a 7.8 percent gain for 2005 compared with the previous year.

Since China joined the WTO in 2001, it has been accepted wisdom that low-priced Chinese labour will undercut western manufacturers, driving them toward extinction. The rule is, you cannot beat the China Price.

Consider the case of Gildan Activewear Inc., a Montreal-based company competing in an industry that many assumed would be dominated by Chinese manufacturers. Gildan makes T-shirts. In 2005, it manufactured almost 400 million of the things. Textiles is labour-intensive industry. How could a company headquartered in Montreal ever survive?

Predictions of Gildan’s extinction, however, have proven to be more than a little premature. The company is doing quite well in the face of the China threat.

Benchmark Global Clothing Price

The textile-and-clothing sector is a big part of the global flow of goods, accounting for some 7% of the total value of goods traded around the world.

Gildan had begun mapping out a defence to the end of quotas nearly six years ago. The company sent a team of employees around the world to study the global price of clothing. The economic emissaries returned with a wealth of data that executives used to determine the benchmark prices Gildan would have to achieve to stay in business as a global producer. In other words, they figured out what was going to be the new price of a cotton T-shirt, and then they developed a corporate strategy based on that price.

“The first thing we did from Day 1 was to make sure that we benchmarked ourselves against the global market,” says Glenn Chamandy, the CEO of Gildan. “We said, ‘This is where we need to set our selling price,’ and every year from then on we started declining our selling prices in anticipation of getting ready for more of a global market. A lot of our typical North American competitors were dissatisfied with us, but we weren’t viewing them as price setters anymore. We were looking at the foreign competitors.”

Offshore Production

Based in Canada, Gildan’s executives realized that if the company was going to be successful, it was going to have to reduce costs–by going offshore.

It did that in 1998 by relocating some of its sewing facilities to Honduras, followed by Mexico, Haiti and Nicaragua. Gildan also built massive state-of-the-art textile processing facilities in Honduras and the Dominican Republic starting in 2001. The company employs some 10,000 workers, most of them sewers, but also local managers who oversee the operation of each hub, which produces some 375 million garments a year. (The company’s facility in Honduras is the largest such operation in the world.) Wages in Gildan’s factories are still higher than those paid in Chinese factories: the average wage of a garment worker in Honduras is about $100 a week–four times what a Chinese worker makes. But the combination of still relatively low wages and advanced technology has allowed Gildan to lower its price per shirt to below that of Chinese manufacturers. “Today, if you look at our basic wholesale product–a white 100% cotton heavyweight T-shirt–we’re selling it for just over a dollar,” says Chamandy. “The costs for a similar landed product from China today would be 10% to 15% higher.”

Take Advantage of Trade Pacts

But it’s not just inexpensive labour and advanced technology that have allowed Gildan to beat the Chinese on cost. Also important for the company has been a close reading of the mass of bilateral and regional trade agreements. By strategically locating its production facilities in certain jurisdictions, Gildan has been able to ensure that it can ship duty-free anywhere into North America, the EU countries and Australia.

Fast Response

Today retailers don’t like to hold stock. Inventory is expensive, and it takes up time and labour. As a result, retailers have pushed that responsibility onto suppliers. The supplier who can deliver it closest to that date and at the right price is the one who gets the contract. Proximity to the U.S. market is an important advantage for Gildan.

In fact, shipping from China adds about 75¢ to every dozen shirts. To fulfill the requirement for fast response, Gildan has built a network of distribution centres in each of its markets, allowing it to quickly fill client orders. The company has vendor management inventory systems that can ship to customers in 24 hours from the time they place their order. “Our cycle time from offshore is three weeks; from China it’s three months in a container,” notes the company. That fast response time is the company’s secret weapon : “Low labour costs are no longer sufficient to ensure competitiveness in a quota-free market. You have to be close to your end user, and you have to have a good logistics pipeline. Lead time is more important than labour cost.“

A western manufacturer beating the Chinese competition, in one of the most labour-intensive industries on earth, at a time when regulatory barriers have just been pulled down? It can’t be done–except, of course, when it is. In fact, by selling to Australia, where Gildan’s market share has been ramping up, the company is now competing in China’s own backyard. It’s a complete reversal. Gildan–in “something of a show of bravado”–has actually contemplated exporting to China.

A committee has been formed for preparation of a comprehensive action plan for development of knitwear industry, which is under crisis after abolition of quota regime.

A transparent mechanism would be implemented to ensure smooth refund of sales tax. Land would be provided on affordable price to knitwear industry in the textile and garment city projects where land is available with other infrastructure facilities at competitive price.

The Export Promotion Bureau (EPB) should launch a market access programme for knitwear industry and besides the US and EU, the market access in ASEAN, China, Japan, Korea and OIC countries can be explored.

Exports

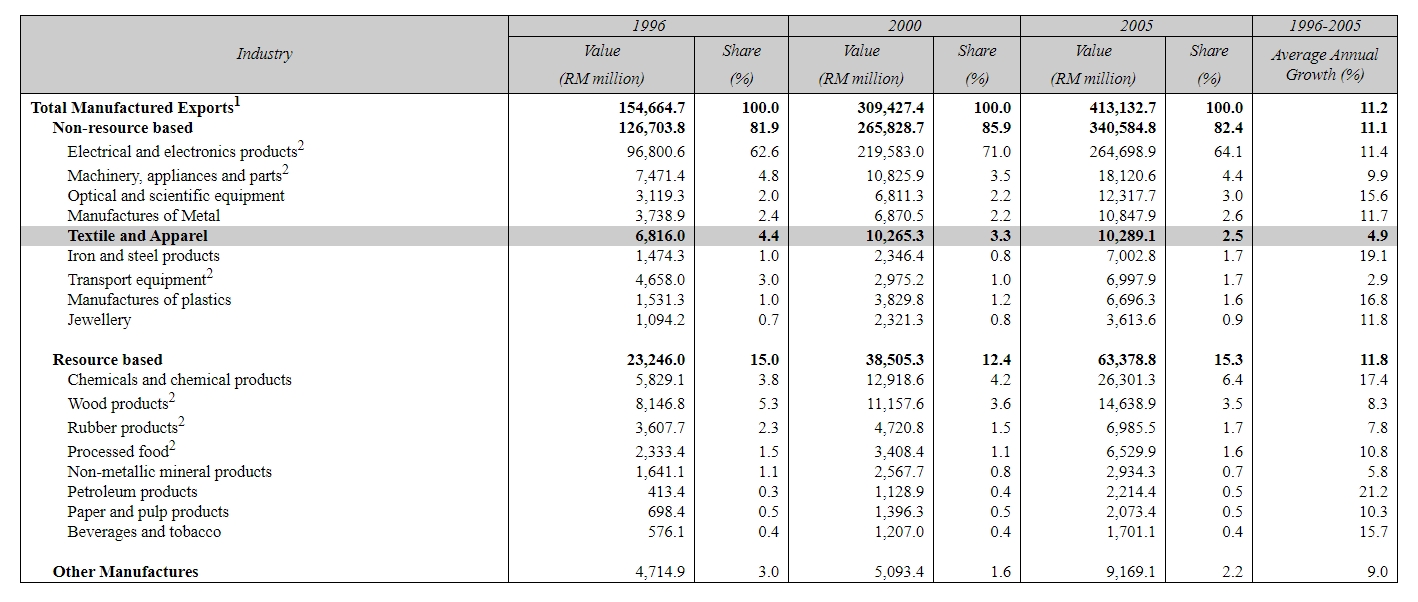

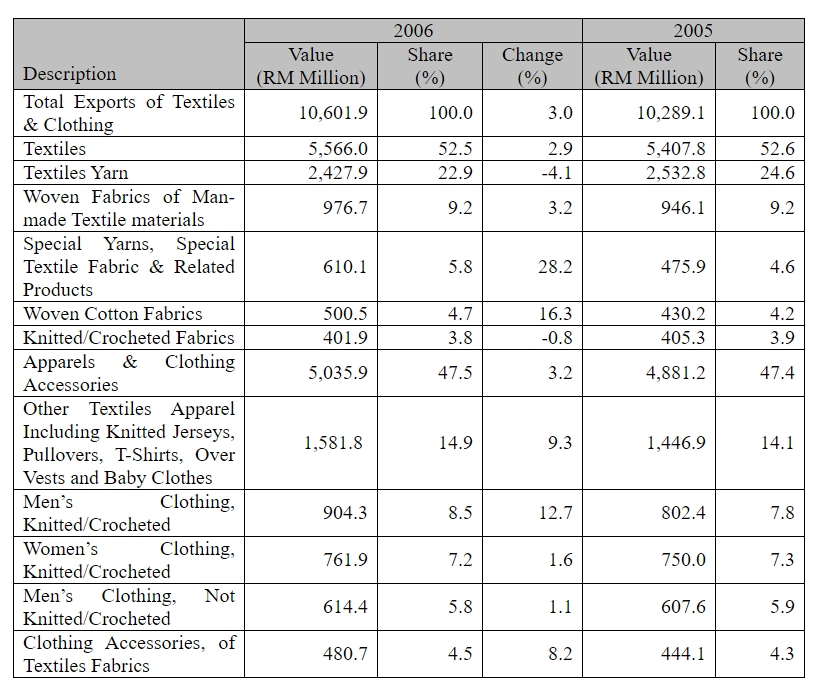

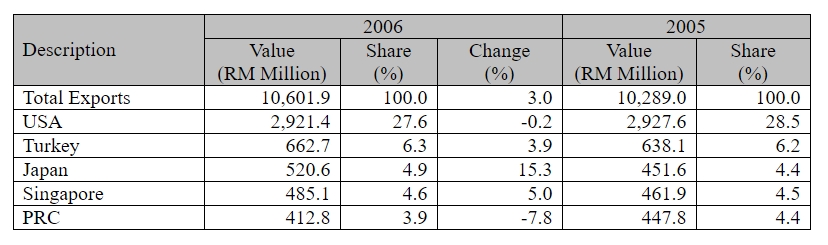

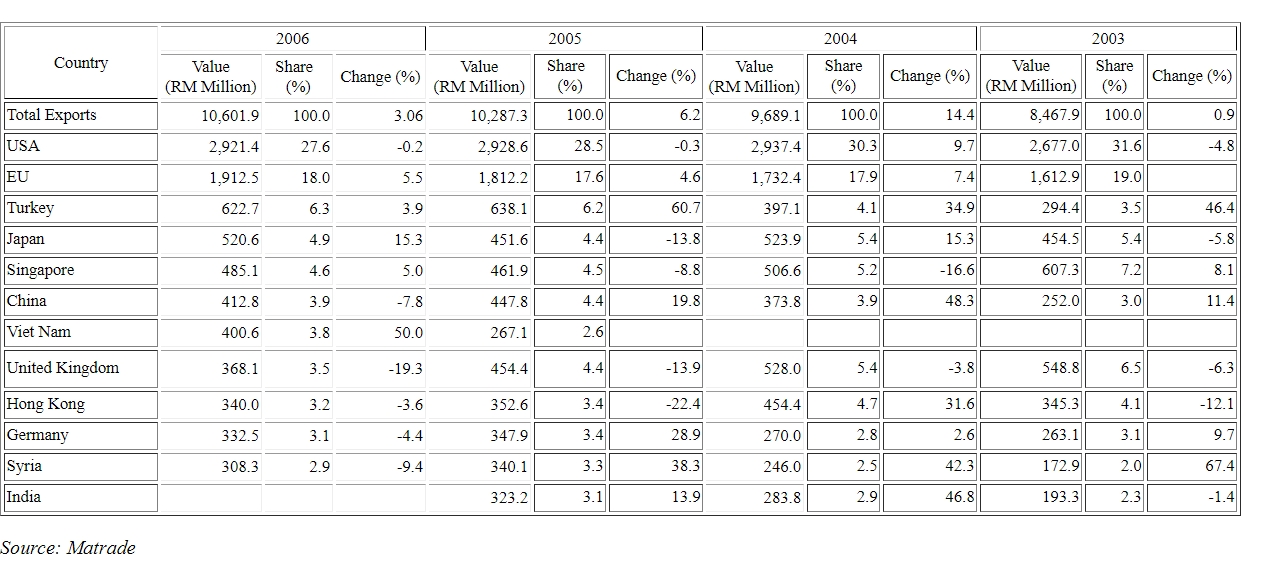

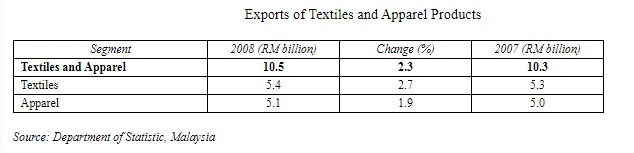

The removal of quotas under the Agreement on Textiles and Clothing (ATC) in January 2005, has changed the international trading environment for this sector. Malaysia’s exports of textiles and clothing remained resilient in 2005, growing by 6.2 per cent to RM10.3 billion.

In addition, the 2005 growth came on top of a 14.3 percent export surge in 2004 valued at RM9.69 billion over RM8.48 in 2003.

Within the sector, exports of textile constituted 52.6 percent of the overall exports while the remaining 47.4 percent comprised of apparels and clothing accessories.

Exports to the major market of the USA, were unchanged at RM2.9 billion and accounting for 28.5 percent of exports of this sub-sector. Exports to the EU increased by 4.4 per cent to RM1.8 billion. Significant increases in exports, in particular textiles, were recorded to other markets, such as Turkey, the PRC, Syria and India.

Turkey emerged as the second largest market with an export growth of 60.7 percent to RM638.1 million followed by Singapore, UK and Japan.

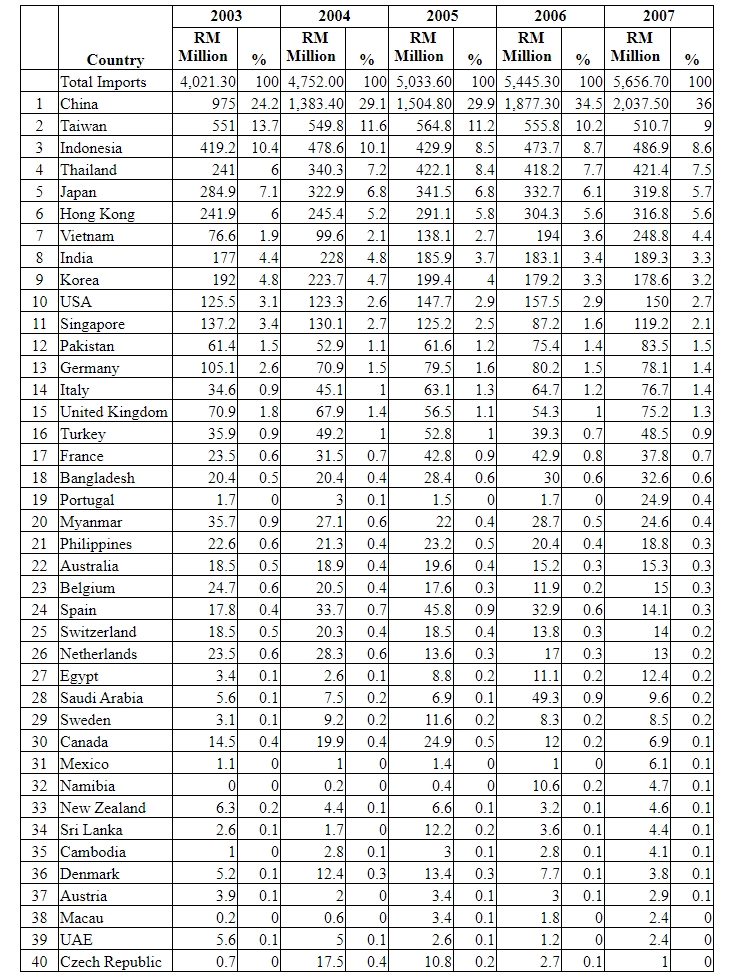

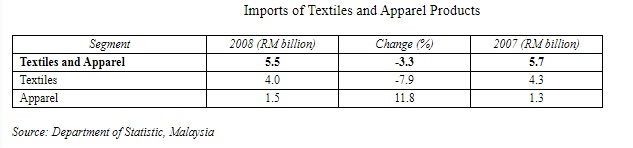

Imports

Total imports of textiles and clothing increased by 4% to RM5.03 billion comprising mainly yarns, woven fabrics and knitted fabrics.

Major sources of imports of textiles and clothing were China with a share of 29.9% of total imports, Taiwan (11.2 percent) Indonesia (8.5 percent) and Thailand (8.4%).

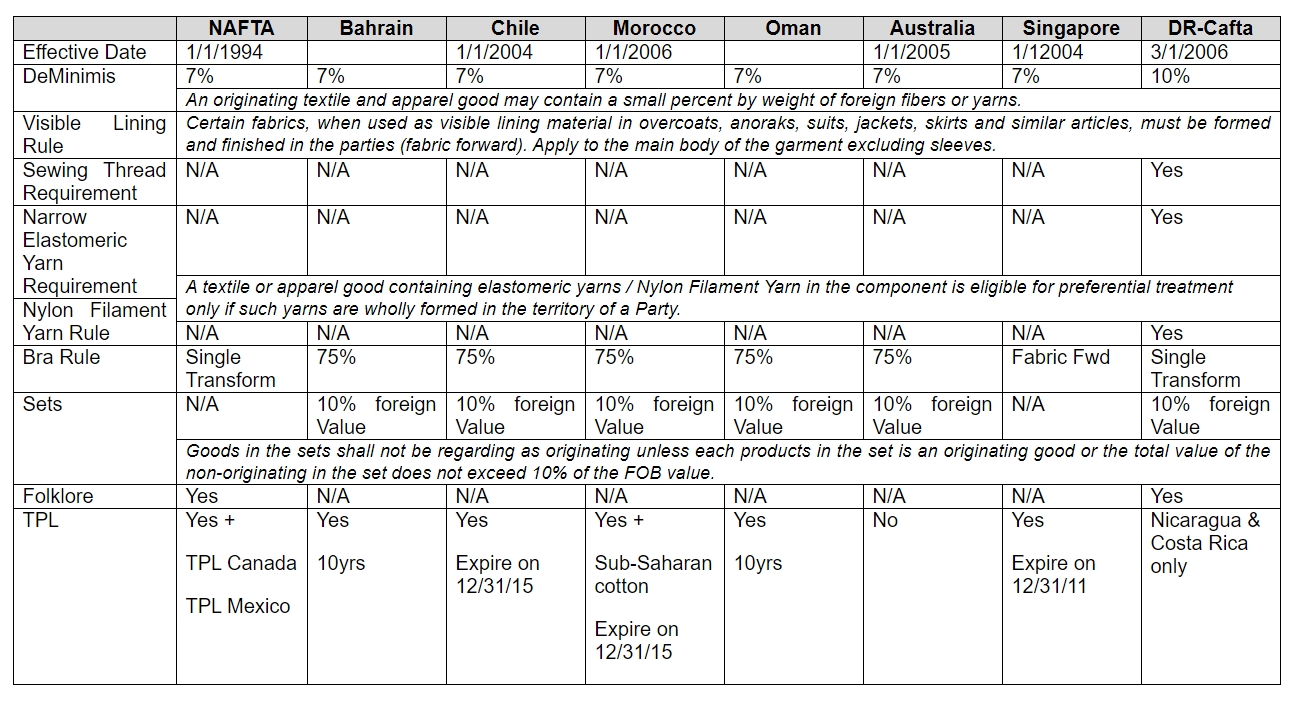

Malaysia and the United States announced the launch of negotiations for an FTA on 8th March this year at Washington. First round of FTA talks are to start in June and the bilateral FTA is expected to be completed by April next year. In line with the Trade Promotion Act (TPA) in the US, the FTA has to be signed before 30 June 2007.

The negotiations were expected to focus mainly on liberalisation of trade in goods, services and investment, including flexibilities and longer phase-in period for sensitive sectors.

USA Current FTA Partners

Country Effective Date / Status

Israel 1-1-1985

NAFTA 1-1-1994

Jordan 17-12-2001

Chile 1-1-2004

Singapore 1-1-2004

Australia 1-1-2005

Morocco 1-1-2006

DR-CAFTA 1-3-2006

(DR-CAFTA covers El Salvador, Honduras, Nicaragua, Guatemala Dominican Republic, Costa Rica, Colombia, Panama, Ecuador)

Bahrain Awaiting Implementation

Oman To be submitted to Congress

Panama Under Negotiation

Thailand Under Negotiation

UAE Under Negotiation

FTAA Under Negotiation

(FTAA =Free Trade Area of the Americas)

SACU Under Negotiation

(South African Customs Union : Botswana, Lesotho, Namibia, South Africa, Swanziland)

Korea Preliminary Discussions

Malaysia Preliminary Discussions

Egypt Preliminary Discussions

Switzerland Preliminary Discussions

Pakistan Preliminary Discussions

MEFTA Preliminary Discussions

(MEFTA=Middle East Free Trade Agreements)

Besides the above FTAs, US also offer special agreements and preference programs with some regional blocs including the followings :

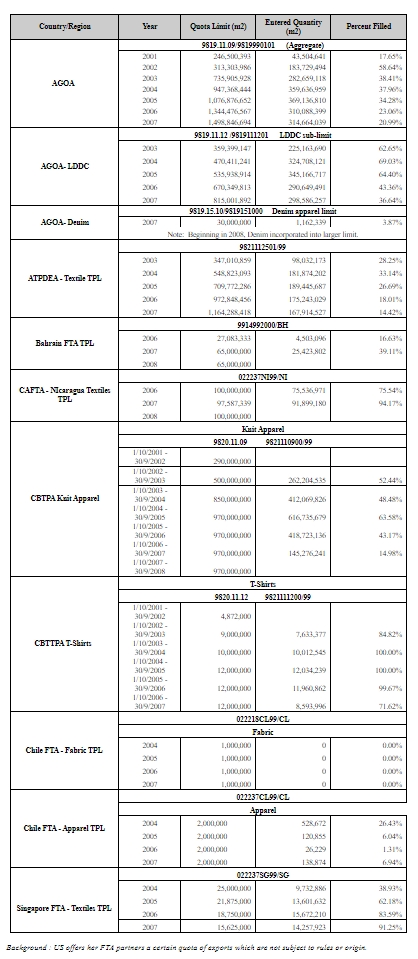

AGOA – African Growth and Opportunity Act (Expire on 30/9/15)

CBTPA – Caribbean Basin Trade Partnership Act (Expire on 30/9/08)

ATPDEA – Andean Trade Promotion & Drug Eradication Act (Expire 31/12/06)

ATPDEA countries include Bolivia, Colombia, Ecuador & Peru.

FTA Creates Competitive Edge

Without quotas, textiles and apparel manufacturers will be searching for a competitive advantage. Without quotas, price will play a major factor in determining who has a competitive advantage. Eliminating duty is one way to reduce the price of a product.

Duty Rates under FTA

Products of FTA countries can be eligible for two or three different duty rates, depending on the inputs (raw material) and production. In regards to the textile and apparel sector, yarn forward is the required rule of origin in most FTAs with US except Jordan & Israel FTAs.

Short Supply

At the request of an interested entity or actual purchaser of a textile or apparel good, fibers, yarns or fabrics not available in commercial quantities among the parties can be sourced from third countries to meet the tariff shift rule.

Tariff Preference Level

Tariff preference level is similar as tariff rate quota (TRQ). A certain quantity of goods can enter during an annual period and receive a reduced rate or duty free treatment even though they do not meet the tariff shift rules. Usually the volume is reduced over a period of time to allow trading partners to integrate.

US FTA Fact Sheet

What is C-TPAT?

C-TPAT is a voluntary government-business initiative to build cooperative relationships that strengthen and improve overall international supply chain and U.S. border security. Through this first worldwide supply chain security initiative, the U.S. Customs and Border Protection (CBP) is asking businesses to ensure the integrity of their security practices and communicate and verify the security guidelines of their business partners within the supply chain. In exchange, CBP provides reduced inspections at the port of arrival, expedited processing at the border and other significant benefits such as “front of the line” inspections and penalty mitigation.

Launched in 2001 with just 7 importers, today 6,000 companies have been accepted as certified partners.

CBP is responsible for screening all import cargo transactions. Utilizing risk management principles, C-TPAT seeks to enroll compliant low-risk companies. The goal is to identify compliant trusted import traders who have good supply chain security procedures and controls to reduce screening of their imported cargo. In turn, this enables CBP to focus screening efforts on import cargo transactions involving unknown or high-risk import traders.

Benefits of Participation in C-TPAT

By participating in C-TPAT, companies will ensure a more secure and expeditious supply chain and benefits including:

CBP expectations for the C-TPAT participant

Certified C-TPAT companies are committed towards the common goal of creating a more secure and efficient supply chain through partnership. Businesses must ensure that their brands, employees, and customers are protected to the best of their abilities.

Foreign Suppliers Requirements

After the importer’s C-TPAT validation, follow-up meetings and site visits are conducted with foreign suppliers and service providers to evaluate their progress against the C-TPAT Security Criteria. As part of this plan to regularly inspect supply chain partners for security compliance, the company will conduct several unannounced on site security inspections. In addition, the company will amend suppliers’ contracts to incorporate minimum security requirements and initiate risk-based audits.

When a C-TPAT certified company out sources or contracts elements of their supply chain, it is imperative that the manufacturer adhere to security measures. The new purchase orders will include the language “Supplier accepts responsibility for factory and container security…..”

International suppliers are required to provide semi-annu al “Business Updates” that include security measures, management changes, employee turnover, policy changes with respect to packaging handling, storage, financial status etc. This information is used to analyze risk, determine contractual compliance, ensure continuity of security measure and need for modifications to security plans.

Only manufacturers who received a passing score in Factory Certification Requirements are permitted to do business with the C-TPAT companies. If a supplier is unable to meet C-TPAT security criteria but is deemed a “critical” supplier by the Company, close scrutinizing the shipments will be conducted to address the supplier’s security vulnerabilities.

Foreign manufacturers will be given formal onsite supply chain security training sponsored by the US C-TPAT certified Company. This training is documented and participants are tested to ensure their understanding of the information taught.

For more information on C-TPAT, please browse the following website :

Textile and Clothing together with electrical and electronic goods, represent the two most dynamic sectors in the global trade. Global export of textiles and clothing during year 2004 were US $453 bn. and of which clothing US $258 bn. Clothing exports which was US $108 bn. in 1990 has increased by 138% during last 14 years.The World Five leading exporters of clothing are China followed by Hong Kong Turkey, Mexico and India. These five Countries accounts for 43 percent of total global clothing exports.

The world five (5) leading clothing importers are European Union, United States, Japan, Hong Kong and Russian Federation. The above countries accounts for 94 percent of total global clothing imports.

With continued increases in world population and global incomes, the textile and clothing industries are expected to grow at 3.2% and 5.3% respectively over the next decade. If the rates of growth are maintained, textile and clothing would be a formidable US $ 600 bn. industry by 2014. (estimates based on 1990-2002 trend by ITCB). The growth promise a potential market share for all efficient producers, including smaller countries who have built reliable long term relationships with their intermediaries.

On 1st of January 2005, the global apparel industry was freed from quota restriction after over 40 years. The elimination of quota also raised the bar, for suppliers, and ability to ship a quality garment on time at a competitive price has became only an entry – level requirement.

The initial trend in the quota free era –

– Increased imports by USA and Japan however decline in EU market due to low consumer spending.

– Continuous dominance of China in textile and apparel trade.

– Emergence of South Asia as an alternative to China as a favoured sourcing destination.

– Exporting from vulnerable countries like Bangladesh, Sri Lanka and Cambodia have increased.

– Prices are down to an extent of 5-8% in almost all the categories.

– Developed Asian countries like Taiwan and Korea and countries dependent on quota have seen fall in exports.

– Leading supply organization in China and selected other countries have seen growth in top line as well as bottom lines.

– Uncertainties regarding safeguard quotas and trade agreements have resulted in buyers/brands, not changing their sourcing destinations to a very large extent.

– Buyers are looking at working on long-term with their vendors than on pure transactional basis.

– It has become a buyer’s market and under pressure from buyers the clothing suppliers are becoming more service providers and offer services that go far far beyond sewing garments.

– Today buyers bring in manufactures of garments at early stage for sourcing to buyers.

The winners and losers in early trends

U.S.A Market

(1) As predicted, China is the major gainer of quota abolishment.

(2) South Asia also has gained market share.

(3) Mexico, AGOA and developed Asian economics are the losers.

In the U.S.A Market, most of the Asian Countries namely China, India, Indonesia, Bangladesh, Pakistan, Sri Lanka, Vietnam, Cambodia etc. has increased their exports to U.S.A Market whereas the Central Latin American and Caribbean country’s, the exports to U.S. Market has decreased during first year of quota expiry. The main countries are Mexico, Honduras, Dominican Republic, Guatemala, El Salvador etc.

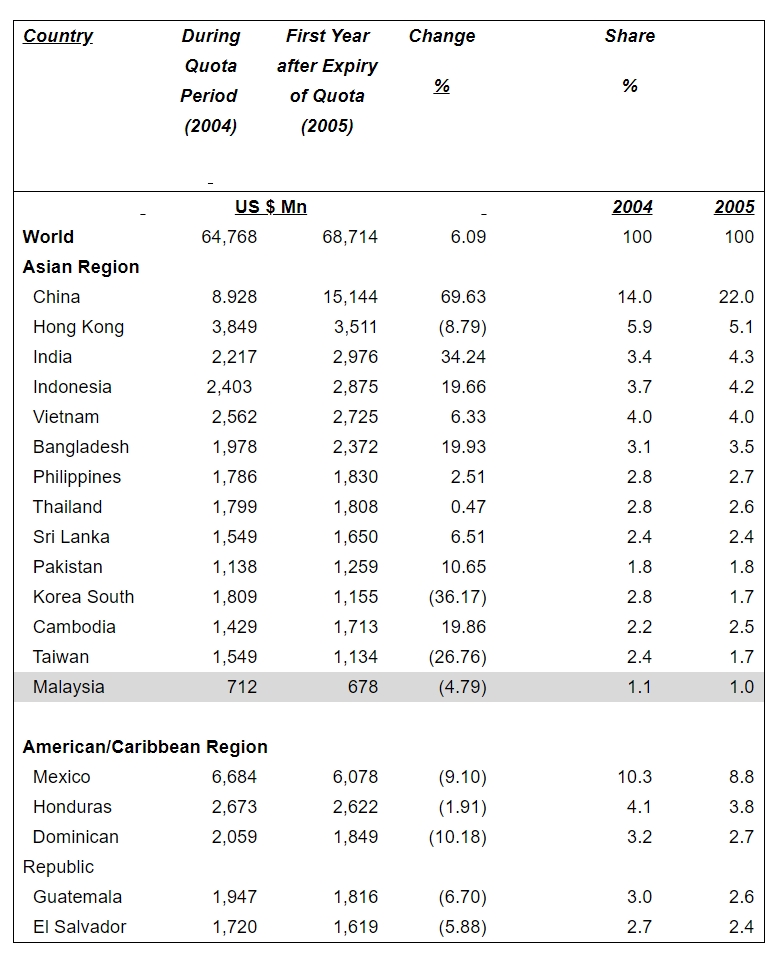

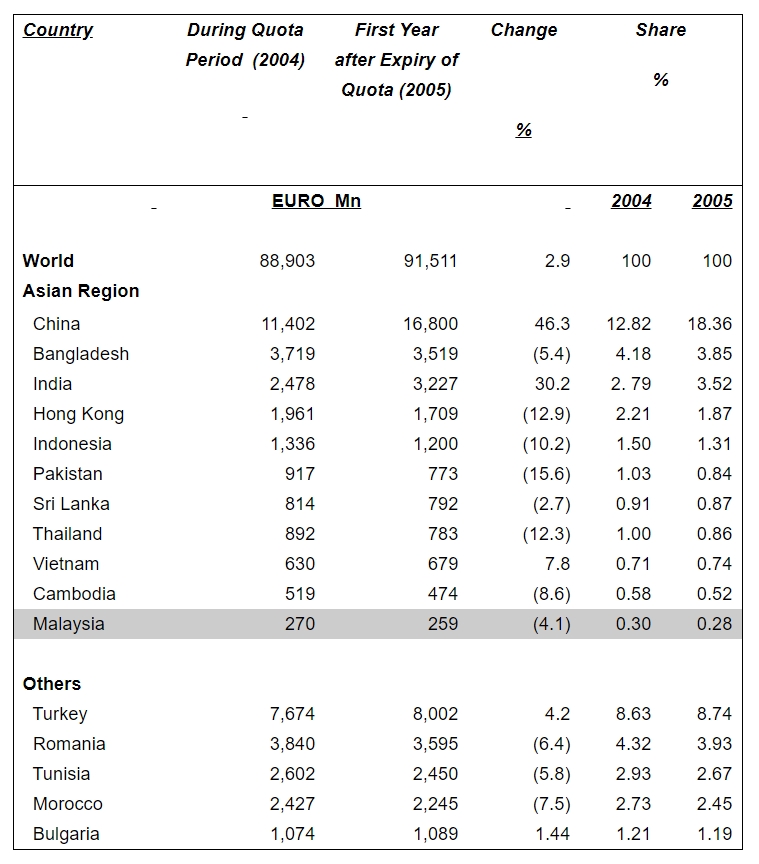

The detail imports between during quota year 2004 and first year after expiry of quota 2005 are as follows.

U.S.A Total Imports

The East Asian countries – Hong Kong, Korea, South and Taiwan shows negative growth mainly because their shifting towards electronics goods as stated elsewhere in the study.

EU Market

(1) China and India have increased their exports in decreasing market.

(2) Turkey and Bulgaria have also increased their exports to E.U.

(3) Countries like Morocco, Tunisia which at totally dependent on E.U Market has lost its share.

In the E.U Market once again only China and India has shown large increases with 46.3% and 30.2% respectively. Most of the other top exporting countries excluding Turkey with increase of 4.2%, Vietnam – 7.8% and Bulgaria mere 1.4%, has shown decline in exports. China is the major supplier to E.U with a share 18.36, followed by Turkey with 8.74%.

The detail imports between during quota year 2004 and first year after expiry of quotas (2005) are as follows.

EU Total Imports

Measures which will limit China growth in next few years

Post-ATC, China has increased it’s share from 14% to 22% in the USA market and from 12.82% to 18.36 % in the EU market during year 2005.

China is expected to gain a major share in world textile and apparel trade however this rapid growth will be hampered due to-

– heavy dependence on imports of raw material – MMF – Yarn and fabrics,

– rapidly growing domestic market – which consumes about 70% of textile and apparel output by volume. Domestic market growing at a rate of 10-12% per annum.

– No countries would depend only on one country for the sourcing requirements.

The countries to benefit from China’s safeguard measures for USA market

Categories Countries to benefit from safeguards

Cotton Shirts Mexico, Honduras, El-Salvador,

(338/339) Guatemala, India, Pakistan, Bangladesh,

Thailand, Sri Lanka, Indonesia and

Jordon.

Woven Shirts India, Bangladesh, Indonesia, Sri Lanka

Men/Boys and Vietnam

(340/640)

Cotton Trousers India, Bangladesh, Cambodia,

(347/348) Indonesia, Philippines Nicaragua,

Sri Lanka, Vietnam, Jordon, Honduras and

El Salvador.

MMF Knit Shirts Guatemala, Jordan, Turkey, Honduras and

(638/639) El Salvador

MMF Trousers Central American Countries, India,

(647/648) Bangladesh, Indonesia, Jordan, Thailand,

Philippines, Guatemala, and Mexico.

As a result of abolishing of quota on trade in textiles and clothing on 1st January 2005, the prices are falling and major western buyers are narrowing their sources. On a global scale, large Asian countries with vertically integrated industries are becoming the world’s leading suppliers. China in particular can produce textile or clothing item, at any quality and cost.

A recent study reveals that in the post quota era, China and India will emerge as the biggest gainers in terms of international market share 50% and 15% respectively in the United States, 29% and 9% in the E.U. The rest of the world is striking, and now South Asia will be the world’s second most competitive region after China.

The study implies that Asian – LDC’s, who has an advantage of quotas will be hardly hit. This implication for countries like Cambodia, Nepal, Bangladesh thus it is, projected to be difficult.

Another study assesses country situations by scrutinizing three forms of costs. Direct Cost (fabric, labour), Indirect Costs (facilities a factory can offer on preproduction, technology aided design assists, sampling labs, efficient communication and sourcing information) and Country Costs (not having duty-free market access, proximity to customers, able human resources, business friendly environment and good logistics). The combination of indirect and country costs is much more important than the direct costs advantages on labour and other items. The clear winners in studies are those that enjoy indirect or country cost advantages or a combination of both (China, India, Turkey, Italy). Potential country cost winners also are those that enjoy preferential access to major market. (Mexico, CAFTA).

Other Factors

Under pressure from buyers the international garment industry is now moving towards as s service industry and what the buyer/retail companies- is used to do yesterday, the garment manufacturer has to do today.

Another country which benefited immensely from tariff preference is Jordon. In year 2000, its apparel exports to USA was only US $ 42 mn. and after spinning the Free Trade Agreement with the USA in 2001, its exports to USA in 2005 has reached US $ 1,083 mn. making a growth of 2,578%. This underscore the fact that countries enjoying preferences have a head start and Asian Countries that are nowhere near to enjoying comparative preferences are disadvantaged. Although Singapore has recently signed on FTA with the United States, its Apparel Industry is insignificant.

The countries that are most competitive by Virtue of Scale, Cost and Capacities and that are vertically integrated with the rest of the production chain including the ability to offer supplementary services.

The countries that are moderately competitive are beneficiaries of tariff preference, Niche expertise and shorter distance to major markets.

Potential exists for even small countries to orient their upgraded capacity towards Niche markets. Eg. Sri Lanka and its world class production of one such Niche item – lingerie.

The sourcing of apparel items also will depend on the type of product. The element of fashion is linked to issues of replenishment. The decisions made by sourcing agents in single season products with limited prospect of replenishment such as women’s dresses, traditional costs and tariffs would be influential, whereas for products requiring in continued replenishment, such as men’s trousers, issues related to lead time, inventory and shorter distance could be influential.

Mounting competition at the distribution end of the pipeline is prompting distributors to shift towards lean retailing, which requires frequent deliveries and continuous monitoring of sales form suppliers, in an effort to adjust product assortments. This is turn makes it imperative for suppliers to build up information channels and obtain access to point-of-sales data.

It is also seen that many Asian manufacturers are moving from (CMT) manufacturing into Free on Board (FOB) and especially, the fully-fledged fashion producers of Asian countries.

It is important for effective supply chain management to take into consideration all conditions that determine competition. Labour cost being only one of them, others are tariffs, transportation, market proximity, infrastructure and services from utilities, environmental impact of production processes, labour standards and in particular lead times.

Comments from Buyers and Suppliers

Buyer

· With quota expired, we are looking at negotiating better prices with our Vendors, however, price is not the only criterion on which we base our sourcing decision.

· Prices have decreased by 5-6% in many categories. This is an ongoing phenomenon. But with quota gone, price competition has become intense.

Supplier

· Most categories have seen a price drop at 5-7%.

· We are experiencing tremendous pressure on margins. Volumes are up but our bottom line is impacted.

· Most of our buyers are increasing orders but also negotiating for a price review.

The garment supplier in the developing countries, now should understand the new rules of the game and learn to play efficiently and effectively if so, to survive in this fast growing industry which is now almost controlled by the buyer.

(The writer is a Chartered Marketer who has over 25 years experience in textile and clothing sector and conduct studies on textile and clothing sector and contribute articles to National and International magazines. E.mail address-ahhsaheed@sltnet.lk or saheed@dialogsl.net )

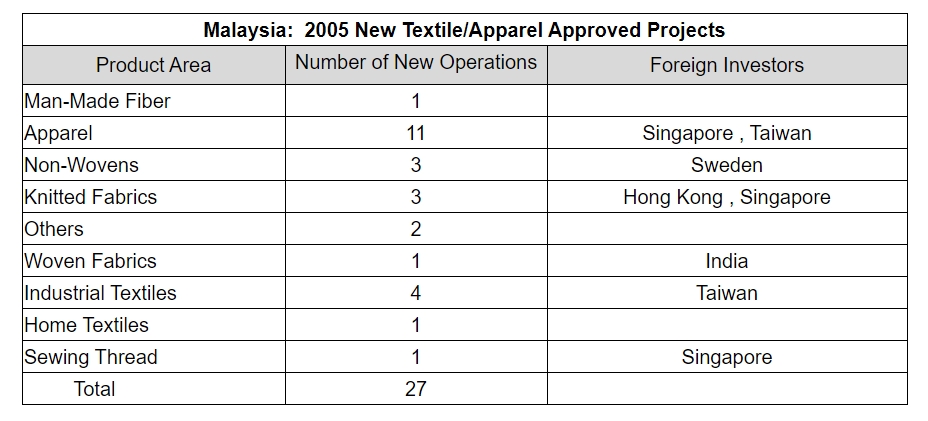

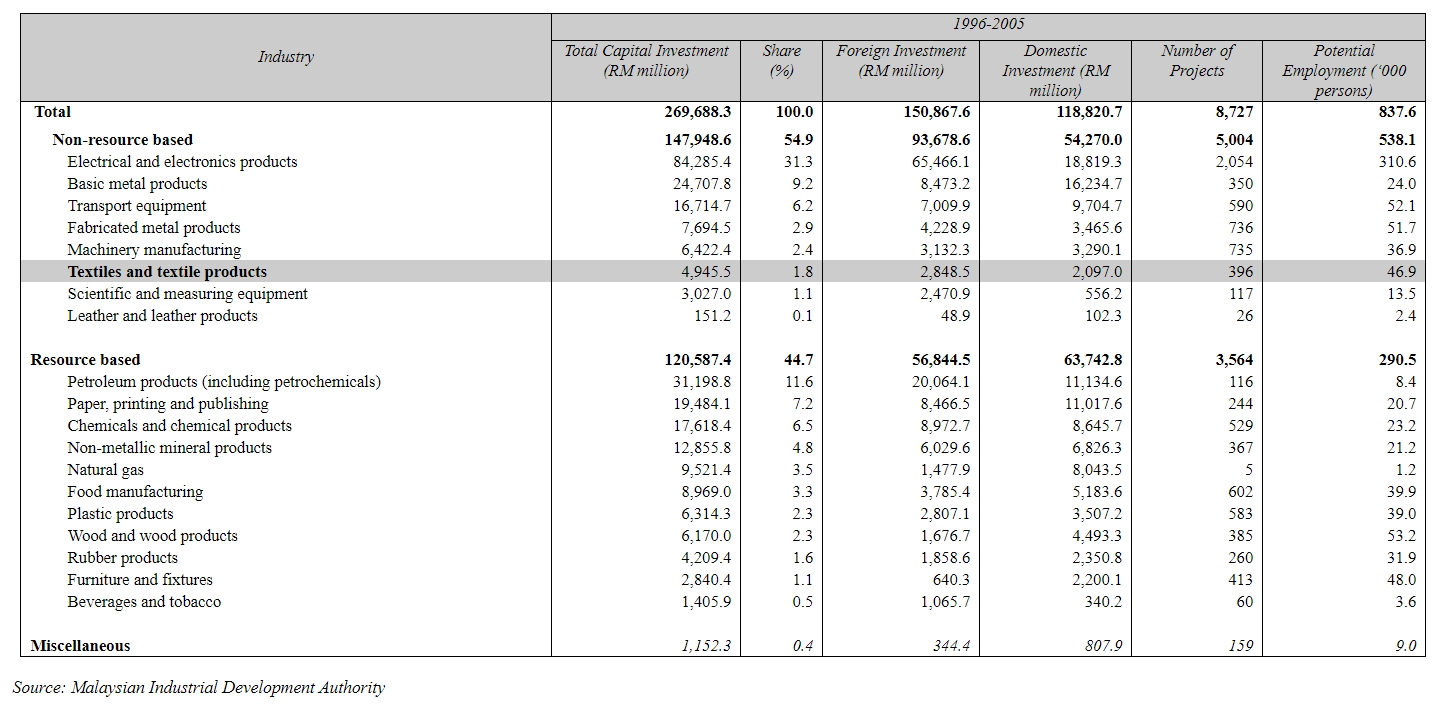

The entire textile sector drew investors in 27 new projects in 2005, with foreign investment from Singapore, Taiwan, Hong Kong, India and Sweden; the largest investment was in apparel followed by industrial textiles.

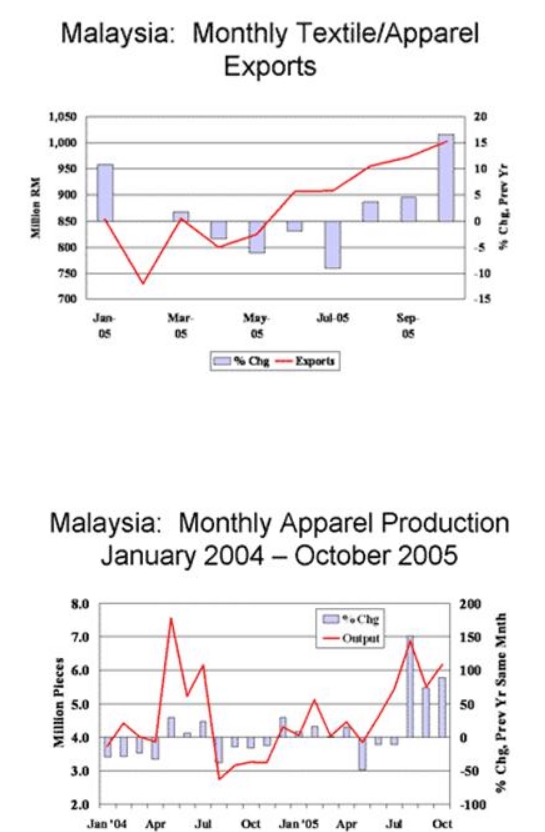

Total textile and apparel production is expanding–first quarter output was up sharply. January output expanded 7.9 percent from the previous year and was followed by a 19.4 percent surge in February. The driver is both domestic sales and exports. January textile, apparel and footwear exports expanded 7.5 percent to RM916.6 million and were followed by a 10.9 percent expansion in February to RM809.1 million. Cumulative January through February exports were up 9.1 percent.

January through February exports to the U.S. market expanded 13.7 percent to 57.39 million square meters. The growth is both in apparel and MMF non-apparel products.

The consumption of cotton appears to be improving, led by an increase in cotton fabric output, which is being absorbed by soaring apparel output. Cotton fabric output fell 10.2 percent in 2005 but is now rebounding. January through February cotton fabric output posted 13.2 percent year-on-year growth, reaching 26.139 million square meters.

In the apparel sector, output experienced 35.9 percent growth in 2005 to 70.193 million pieces. This has been followed by January through February 2006 cumulative expansion in output of 46.6 percent, reaching 13.444 million pieces. Malaysia has proven successful in boosting its apparel exports to the Islamic markets; exports to Turkey, Syria, Egypt, Pakistan and the United Arab Emirates are rapidly expanding.

China’s very influential National Development and Reform Commission have released its new five year plan and goals for the textile and apparel industries. Since the textile and apparel sectors are now privatized, the plan is a reflection of government policy towards the industries. Overall, the new five year plan for 2006 through 2010 will emphasize a move from a focus on quantity to quality.

It is interesting to note that higher quality exports will be encouraged with 2010 textile and apparel exports targeted at 750 billion U.S. dollars, representing a 50 percent increase over the levels of 2005.

The plan will include:

* Improvement in textile machinery and technological products.

* Buying international brands.

* Create own brands.

* Using optional fibre.

* Reducing the use of energy sources.

* Speeding up reform of state-owned textile enterprises.

* Promote innovation in technology.

* Set up several huge textile parks in various provinces.

Key Points of the 5-Year Development Plan

~ Improve quality, switch to value added products and develop brands.

~ Increase textile/apparel exports by 50% by 2010 to 750 billion U.S. dollars.

~ Spinning output growth upgraded at 6% annually through 2010. Total domestic consumption of fibers targeted at 36 million tons by 2010.

~ Domestic textile/apparel sales target to increase 12.7% annually.

~ Total annual fiber output increase from 15.29 million to 24 million tons.

~ Total yarn output to expand 5% annually from 14.4 million to 18.5 million tons.

The US Customs and Border Protection (CBP) has recently issued an informed compliance publication (ICP) entitled “What Every Member of the Trade Community Should Know About: Marking Requirements for Wearing Apparel”. The ICP provides guidance and useful information on the marking requirements for textile and apparel articles imported into the US.All wearing apparel items must be marked with the name of the country of origin by means of a fabric label. In the case of garments that cover the upper torso such as shirts, blouses, coats, sweaters, dresses and similar apparel, country of origin marking must be placed on the “inside center of the neck midway between the shoulder seams or in that immediate area”.

Trousers, slacks, jeans, shorts, skirts and similar wearing apparel must be marked by means of a permanent label affixed in a conspicuous location on the garment, such as the inside of the waistband.

The Federal Trade Commission (FTC) is responsible for enforcing the Trade Regulation Rule Concerning the Care Labeling of Textile Wearing Apparel, which requires a permanent label that provides care instructions on all wearing apparel, unless there is an exemption (e.g. gloves).

Gloves

Customs has held that bulk packages of work gloves (usually 1 dz. pairs to a poly bag), which are given to employees, may be excepted from individual marking provided that the gloves in outside containers (poly bags) properly marked with the origin of the gloves. Gloves that are not contained in a poly bag but are fastened only by a paper band which may easily become detached or ripped from the gloves, may not be excepted from individual marking. However, Customs has held that cloth work or garden gloves may be marked to indicate the country of origin by means of a heavy paper folder which securely fastens the gloves together. Gloves may be marked with a hang tag instead of sewn-in labels or ink stamps.

Textile Fiber Identification Act

Textile and apparel articles imported into the United States are required to be marked or labeled pursuant to the Textile Fiber Products Identification Act. These acts are enforced by the Federal Trade Commission (FTC). The following are some of the information to be included in English:

• Fiber content, by percentage in descending order by weight, using generic fiber names

• The name of the country of origin of the product

• The name of the importer, distributor, retailer, or foreign manufacturer

• The responsible firm may be identified by its trademark name, provided that the trademark name has been registered with the U.S. Patent Office and a copy of the trademark registration has been furnished to the FTC prior to its use.

For details, please browse the following web :

http://www.cbp.gov/xp/cgov/toolbox/legal/informed_compliance_pubs/

The Japan-Malaysia Economic Partnership Agreement (JMEPA) came into force on 13 July 2006 . With the implementation of JMEPA, products entering Japan on 13 July 2006 and thereafter, that are eligible for preferential tariffs will have to be accompanies with a Certificate of Origin ( Form MJEPA ) endorsed by the Ministry of International Trade and Industry. For textile and apparel products, tariffs are eliminated with immediate effect.

Rules of Origin for Textile and Apparel Products

Procedure to Obtain Preferential Tariff

1) STEP 1: Application for product cost analysis.

1.1) Documents to be submitted:

i. Application Letter;

ii. Completed forms MJEPA 1, MJEPA 1A, MJEPA 2, MJEPA 2A; ( These Forms can be downloaded from MITI website or obtained at MITI office/branch counters.)

iii. A certified true copy of Company Registration Certificate (Form 9)/(Form D);

iv. A certified true copy of raw material invoices;

v. Product sample/Catalog/Picture;

vi. Processing Flow Chart

1.2) Processing of the application is within 7 working days from the date of completed application received.